Group Assets (RRSPs, TFSAs, Non-Registered)

A Group Savings Plan is an employer-sponsored savings plan, similar to an individual account, but administered on a group basis by the employer.

Contributions made to the plan are often matched by the employer however they are not mandatory. Contributions by the employer are taxable as income to the employee. In the case of a group RRSP, the employer's contributions to the RRSP are included in the employee's income but are then deducted as part of the RRSP contribution deduction.

In this article:

- 1

-

Add a new Financial Asset for the Group account on the Assets page

Select Scenario Setup -> Assets.

Under the Financial Assets section, under the Assets tab, click Add Financial Asset.

Each column heading has a question mark that can be clicked for further information on the required fields. Make sure to enter all of the information for the Group Asset including the asset allocation.

- 2

-

Enter the employer and employee contribution percentages under Employer Matching

Select the Employer Matching tab above the table.

Under the Employment Income column, select the appropriate income to link the contributions to. Enter the annual Employee Contribution and Employer Contribution as a percentage of that employment income. You can't enter these percentages until you have linked the employment income.

Employer and employee group contributions can currently only be entered as a percentage of Employment Income using the Employer Matching functionality. To input a group contribution as a dollar value, change the percentage over time, or to set a cap on contributions at a specific dollar amount, please contact the support team for assistance.

On the Planning page, the Group Asset shows the automatic employee and employer contributions as a percentage of the selected Employment Income. Note that the contributions are not editable on the Planning page. Edit contribution amounts under Scenario Setup -> Assets -> Employer Matching.

A client's group contributions to RRSPs and TFSAs will be limited by their RRSP and TFSA contribution room. Snap will proportionately decrease employer and employee contributions to stay under the contribution limit.

In this example, the client has only $7,000 of TFSA contribution room in the first year. Even though we have entered a 5% contribution based on $100,000 of employment income for both employee and employer, Snap constrains the TFSA total contribution to $7,000.

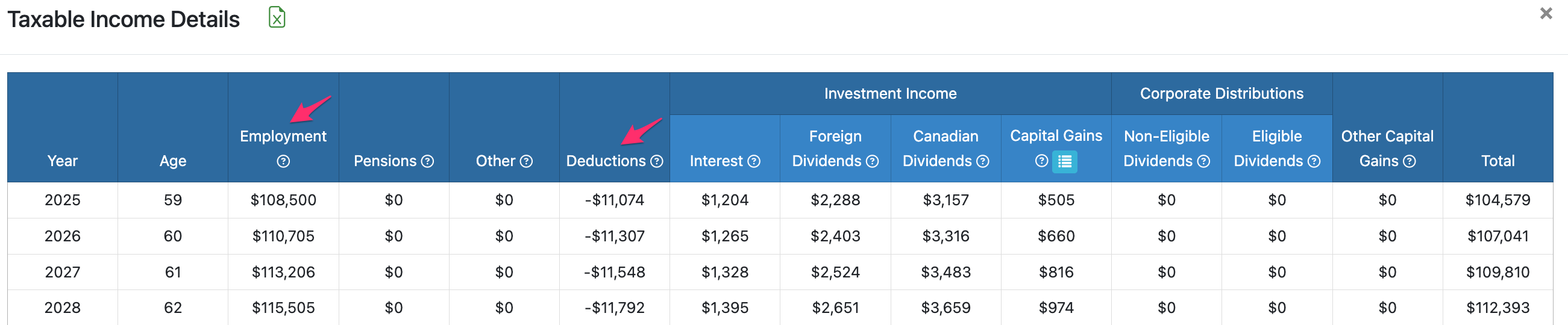

To view the taxable income for the client in detail, click the blue icon at the top of the Taxable Income column.

The Employment Income displayed in this table includes the taxable employer contributions to the Group Assets. For Group RRSP accounts, Contributions are shown as part of the Deductions column. As shown in the example above, in the first year of the projections, there is a $3,500 employer contribution to the Group TFSA and a $5,000 employer contribution to the Group RRSP. The $100,000 Employment Income has been increased to $108,500 as a result and you can see this under the Taxable Income Details table below. The employer and employee contributions to the RRSP total $10,000 which are displayed as part of the Deductions column.