Frequently Asked Questions - Corporations

In this article:

- What is the Other Income column used for?

- How do you enter inter-corporate dividends?

- How do you enter the proceeds from selling a business at a future date?

- What happens to the Corporate Net Worth of a client if a spouse outlives him/her in the projections?

- How can you model corporately owned Term Life Insurance?

- Does Snap track the Refundable Dividend Tax on Hand (RDTOH)?

- Why does it take a few years to fully deplete the Corporate Assets when paying out eligible or non-eligible dividends?

- 1

-

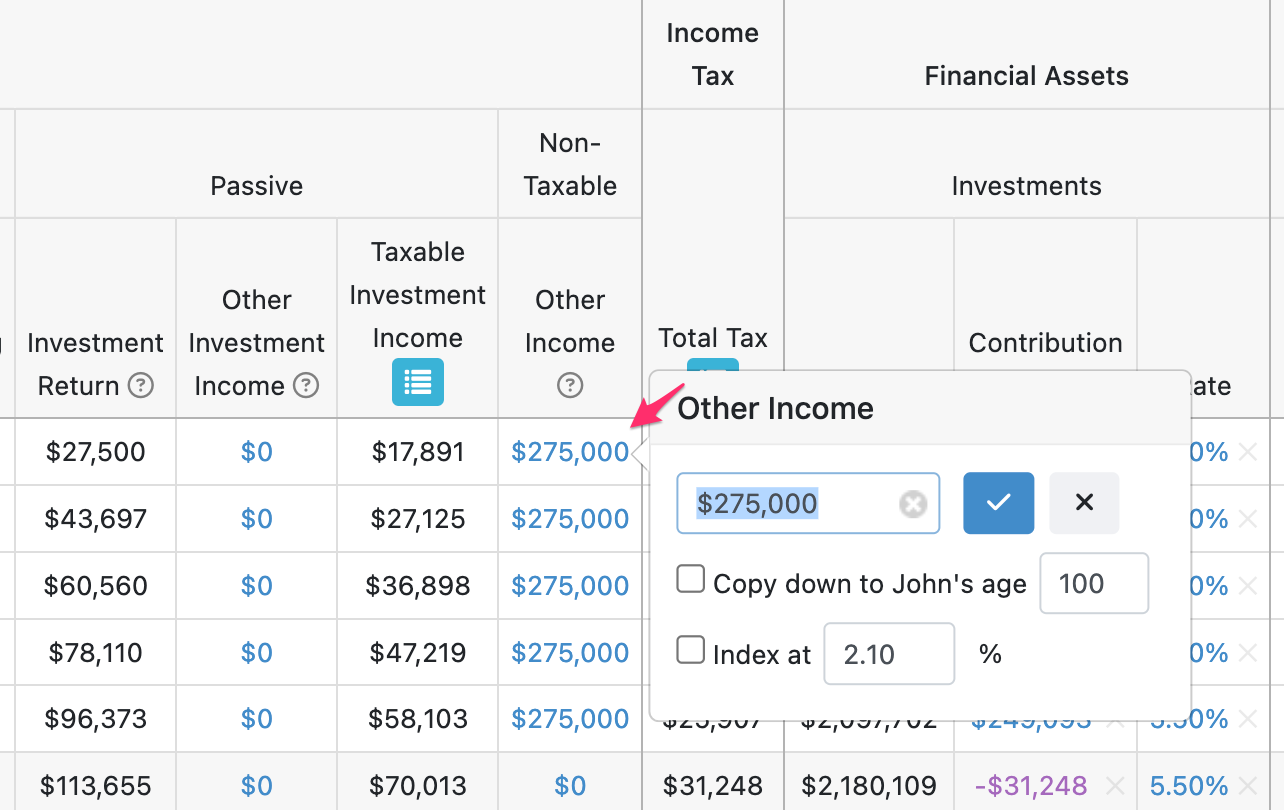

What is the Other Income column used for?

If you want to add non-taxable cash flow into a corporation (e.g., to invest in the Financial Assets) you can use the Other Income column. This column is useful to handle any other non-taxable income (e.g. intercorporate dividends received from a connected corporation tax-free, after-tax proceeds from real estate disposition, or after-tax proceeds from any other corporate asset disposition or an insurance payout).

- 2

-

How do you enter inter-corporate dividends?

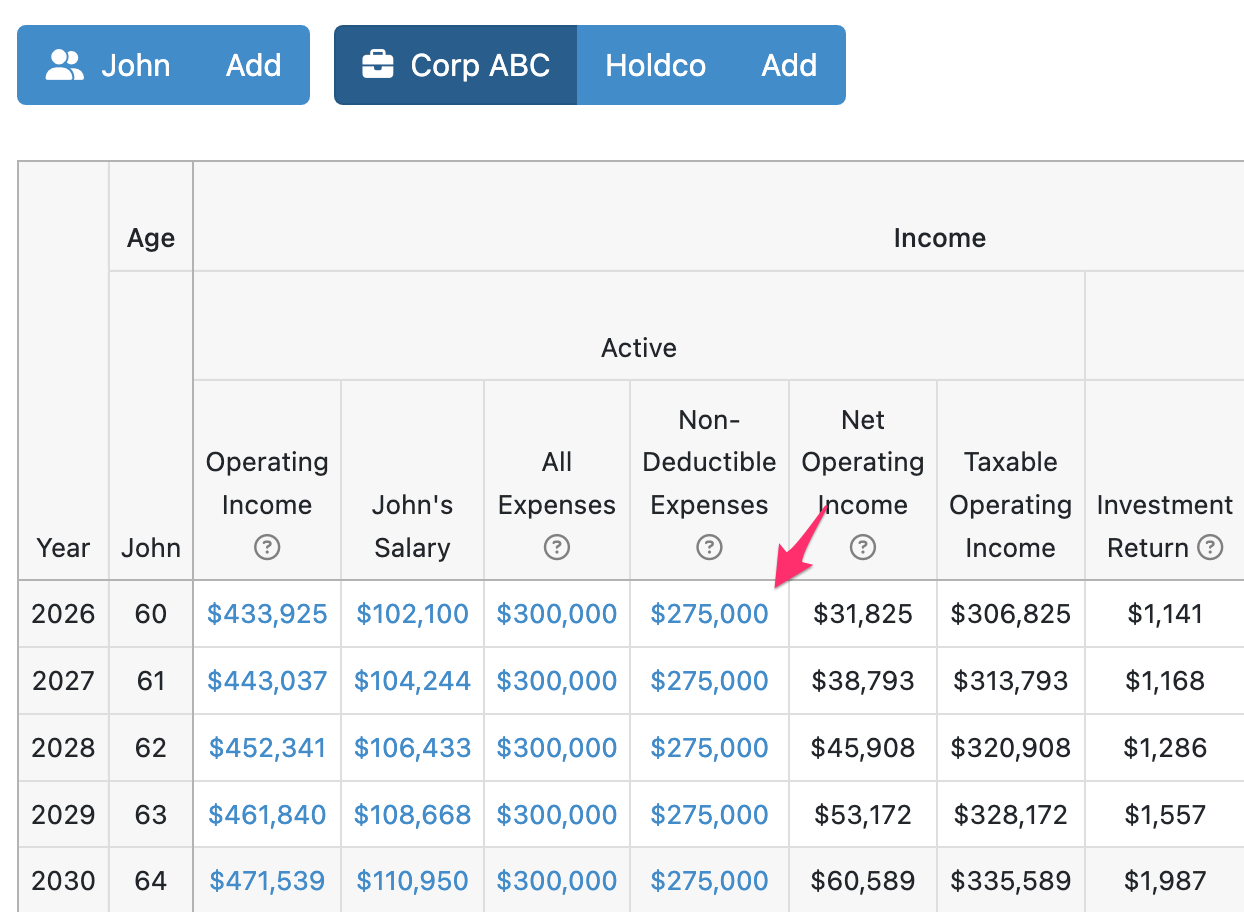

It isn't necessary, or recommended, to show 2 separate corporations for the Opco and Holdco. Instead, you can have both modelled within the same corporation. When there is active business income, this is taxed separately from the investment income. There are other advantages of modelling them together including the addition of GRIP balance if the Opco earns income above the small business deduction amount or if the Holdco has passive income greater than $50,000 in a year (which would impact the Opco's small business deduction limit). These are all factored into Snap if they are modelled together.

However, if you would like to keep them separate and show a transfer of funds from the Opco to the Holdco we can look at each individually. For the Holdco, enter the transferred money under the Other Income column in the appropriate year.

The value entered under Other Income is considered non-taxable income (e.g. tax-free dividend income received from a connected corporation, after-tax proceeds from a real estate disposition, or after-tax proceeds from any other corporate asset disposition).

For the Opco, enter a Non-Deductible Expense to move money out of that corporation.

- 3

-

How do you enter the proceeds from selling a business at a future date?

Option 1: Sale of Real Asset in the Personal Projections

If you expect to sell a personally owned corporation in your projection, you do not necessarily need to use the corporate module for this. You could instead model the corporation as a personally owned Real Asset with a Future Sale Age. This will allow you to control the future sale price (through the Value and Appreciation settings) and the taxes payable through the Cost field. If the transaction will be eligible for the Lifetime Capital Gains Exemption (LCGE) you can add this figure to the Cost to reduce the calculated capital gain.

Option 2: Sale of Real Asset in the Corporate Projections

Option 3: Using the Share Sale method of Corporate Disposition

If you'd like to model the use of the corporation before selling it in the projection (e.g., modelling Active Business Income, Expenses, Salary, and Dividends) you can model this using the corporate module and then enter a Disposition Time of the year the client plans to sell the corporation. The sale proceeds will be received in that year in the personal projections. If you choose this option, under the Scenario Setup for the corporation, enter the Disposition Method of Share Sale and the appropriate Time.

- 4

-

What happens to the Corporate Net Worth of a client if a spouse outlives him/her in the projections?

The Corporate Net Worth of the client is transferred to the spouse upon the client's death. At that point, the Corporations column in the spouse’s projections will show the combined (client and spouse) Corporate Net Worth as dictated by the percentage ownership.

- 5

-

How can you model corporately owned Term Life Insurance?

You can model corporately owned permanent insurance as shown here: Corporate-Owned Life Insurance. For term policies, you can use the same functionality and set the Death Benefit and Premium amounts equal to zero once the term expires.

- 6

-

Does Snap track the Refundable Dividend Tax on Hand (RDTOH)?

Yes. RDTOH is a federal mechanism available to Canadian-controlled private corporations (CCPCs) that allows, under certain circumstances, for a corporation to be refunded a portion of income tax paid.

The RDTOH is segregated into 2 portions as per the 2018 budget; Eligible RDTOH, and Non-Eligible RDTOH.

Both RDTOH account balances are tracked annually (typically with the corporate tax return), and when dividends are paid out to the shareholder(s) of the corporation and if the RDTOH balance is positive, the corporation receives a dividend refund from one of these accounts depending on the situation.

Eligible RDTOH

Payment of a taxable dividend (Eligible or Non-Eligible) will entitle the corporation to a refund from this account. The Eligible RDTOH account tracks refundable taxes paid under Part IV on eligible portfolio dividends.

Non-Eligible RDTOH

Refunds from this account will be obtained only upon payment of Non-Eligible Dividends. The Non-Eligible RDTOH tracks the refundable taxes paid on investment income (Part I tax) and non-eligible portfolio dividends (Part IV tax). If the Non-Eligible RDTOH balance is zero, the corporation can obtain a refund from the Eligible RDTOH account when paying out Non-Eligible Dividends.

To make it easy to take advantage of RDTOH, the balances are tracked automatically in Snap Projections. The balances are calculated based on your selected corporate portfolio settings (available on the Scenario Setup -> Settings -> Portfolio page) and the corporate asset mix (available on the Scenario Setup -> Assets page) and updated based on dividends declared from the corporation.

Non-Eligible RDTOH is generated when the corporate assets are comprised of Cash, Fixed Income, and Equity with the Equity Allocation settings excluding any Canadian Dividends. If the Equity asset class allocation has any Canadian Dividend allocation, you will see Eligible RDTOH generated. Canadian dividend-producing stocks are Eligible Dividends, but foreign dividend-producing stocks are Non-Eligible Dividends.

RDTOH affects only investment income generated by the corporation and it does not impact the remaining corporate component's functionality; including the active business income section.

This means you can generate both Active Business Income and Passive Investment Income in one corporation and both income streams will be taxed separately. That way, in Snap Projections, a corporation can act as a Holding and an Operating company at the same time, and you do not have to resort to setting up multiple corporations to model active and passive business income separately.

If you are aware of the existing balances for Eligible RDTOH and Non-Eligible RDTOH, you can enter these into the software. When entering a corporation for the first time, you have the opportunity to indicate the balance for each account. To edit an existing corporation and enter the balances, select Scenario Setup -> Corporation.

Then enter the existing balances.

- 7

-

Why does it take a few years to fully deplete the Corporate Assets when paying out eligible or non-eligible dividends?

The reason that the Net Worth of the corporation does not fully deplete in one year has to do with certain assumptions that we have built into the calculations in Snap. In a year where a Non-Eligible or Eligible Dividend is paid out, if there's Refundable Dividend Tax On Hand (RDTOH) remaining then a dividend refund is generated which can be applied in the following year in the projections. We implemented the logic that way to stay consistent with other corporate calculations in the software and to avoid circular calculations which would have been created if the refund was allowed to be paid out in the same year. This means that you won't be able to fully deplete the corporate Net Worth by paying out a Non-Eligible or Eligible Dividend in one final year (if there is any RDTOH). The corporation will take a few years to wind down (as shown below).

If you prefer to show the Net Worth being depleted in one final year, you can do the following.

On the Scenario Setup -> Corporation page, you can change the Disposition Time of the corporation to a specific year of the projection. This will liquidate the entire corporation and distribute the after-tax proceeds through a combination of Return of Capital, Capital Dividends, Eligible Dividends, and Non-Eligible Dividends. The taxable dividends are added to the client's Taxable Income in the disposition year.

Alternatively, you can use the following approach. Allow the Capital Dividend Account to build up and don't pay a Non-Eligible or Eligible Dividend in the final year. Instead, pay out a Capital Dividend in that final year to fully deplete the Net Worth.