Tracking savings and withdrawals in an RESP

Although education savings are not part of retirement planning in general, you may wish to track an RESP account within the projections. You can add one or more RESP accounts to the projections and track personal savings towards education, grants that would be applied, the projected balance of the account, and finally the withdrawals which go directly to the beneficiary for education purposes and do not affect the client's cash flow.

In this article:

- 1

-

How to add/edit RESP in your projections.

| To add a new RESP, select Scenario Setup -> Education, then Add RESP. |

|

| To edit an existing RESP in your scenario, select the pencil icon under Actions. |

|

- 2

-

Entering RESP details.

Once you click on the Add RESP button, you will be taken to the Education Savings module where you can provide additional details.

Current Value: The current value of the account is considered to be the value of the account on January 1st of the first year of projections.

Subscriber: For the purposes of Snap Projections, the subscriber is the person who will be contributing to the account. The annual RESP contributions are subtracted from this person's cash flow in the projections. Note that this could be different than the RESP subscriber in actuality. Click here for details on modeling extra contributions from 3rd party sources such as grandparents.

Auto Contribution: By checking this box, Snap Projections will automatically calculate and display a contribution to the RESP that will attract the maximum grant for that year (not including CESG catch up). This calculation is done for all beneficiaries.

Auto Withdrawal: By checking this box, Snap Projections will automatically calculate and display a withdrawal based on the education cost projected for that year. This cost is based on the value and years of education you entered when creating the RESP.

Beneficiary Date of Birth: This is required to determine the contribution timeline. You will see the age of each beneficiary displayed on the RESP details page, and on the Planning page when you hover over the RESP account in that year as shown above.

Beneficiary Claimed CESG: Enter the amount of CESG already claimed by this beneficiary up to the beginning of the first year of projections. This allows Snap to determine the remaining CESG available, and whether future savings to the RESP will attract more grants. This amount is also used to assume past contributions made to the RESP for this beneficiary. For example, if $2,000 of CESG has been claimed, Snap will assume there were $10,000 of past RESP contributions made for this beneficiary since each $2,500 contribution attracts $500 of CESG. Each beneficiary is limited to a total contribution of $50,000.

Education Cost: Enter the amount that you would expect the beneficiary to withdraw for one year of education, in today's dollars. This is used to project an annual cost of education over the years based on what it would cost today (including food, accommodation, tuition, etc.).

Cost Inflation: The annual education cost will be indexed by this percentage every year.

Years of Education: Enter the number of years that the beneficiary will require the amount under the Education Cost column.

Note: If you have not selected the Auto Withdrawal checkbox, the columns in the table for Education Cost, Cost Inflation, Start Age, and Years of Education will not be displayed.

- 3

-

Reviewing RESP on the Planning Page and updating contributions/withdrawals.

On the subscriber's Planning page, you can review and modify the RESP contributions and withdrawals as desired.

You will see the year-end Value of the RESP account to monitor how it grows and depletes with time.

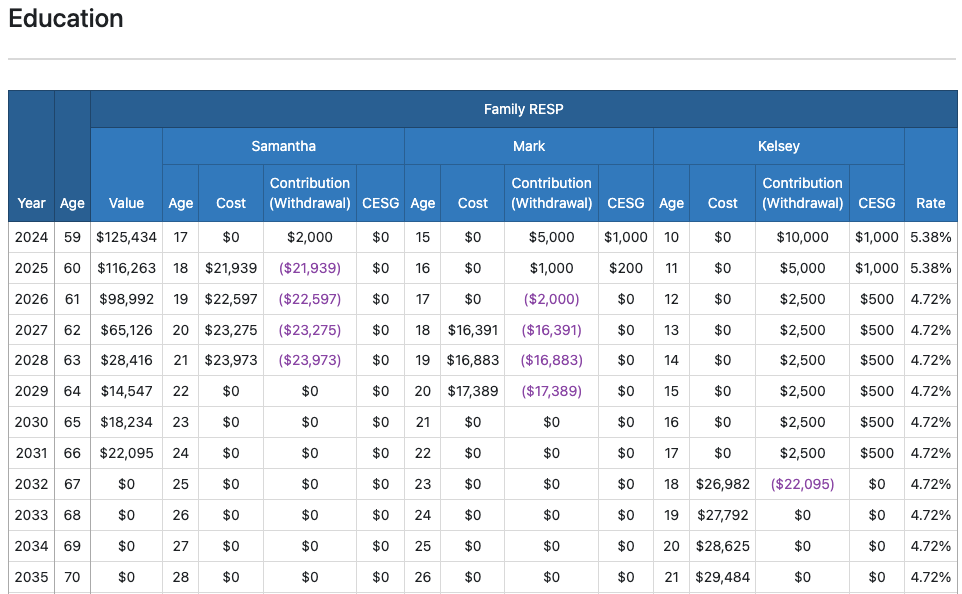

If you opted-in for automatic contributions/withdrawals in Scenario Setup, you will see an automatic contribution of $2,500 to attract the grant of $500 for that year for the 2 children with the remaining grant room and as the children age, you will start seeing automatic withdrawals for their education.

You may wish to increase the automatic contributions for a given year. Default contributions to attract the CESG each year and withdrawals based on the education cost and duration are displayed in the screen capture above. Here is an example to show how to increase the contributions to attract a catch-up for the grant if it is available.

Edit the annual contribution by clicking on the value in the Contribution column. All edited amounts will be displayed with a yellow background. If CESG catch-up is available, the amount in the CESG column will be updated. You can see below that in the first year of the projections a $2,000 contribution for Samantha does not provide any further grant because her grant has already been maximized (as indicated in the Education module settings). However, for Mark and Kelsey, the $5,000 and $10,000 contributions do attract an additional $500 CESG for each child to a maximum of $1,000 in that year. You can read more about the CESG catch-up here. A maximum of $50,000 of contributions to the RESP per beneficiary is enforced.

To show withdrawals from the RESP, enter a negative value under the Contribution (Withdrawal) column.

As mentioned above, you can also change the asset mix and the rate of return for the RESP by clicking the value under the Rate column and editing the Asset Allocation or Rate of Return for Cash, Fixed Income, and Equity.

For Kelsey's education needs in this example, the projected education cost in her last 3 years of education is greater than what is available in the RESP. The software will not make withdrawals from other assets automatically to cover this shortfall. If the parent expects to cover the remainder of the education costs in those years, you could show an additional expense for this in the projections. You can read more about withdrawing funds from the client's assets to supplement the available RESP funds here.

If there is money remaining in the RESP after all automatic withdrawals, you can enter a manual withdrawal in the final year of education to deplete the account. All withdrawals are assumed to flow out of the projections (not into the cash flow of the subscriber).

| You can collapse the Education section on the Planning pages to see a summarized view. It will show you the Total Contribution/Withdrawals for all beneficiaries across all RESP accounts for the subscriber. |

|

- 4

-

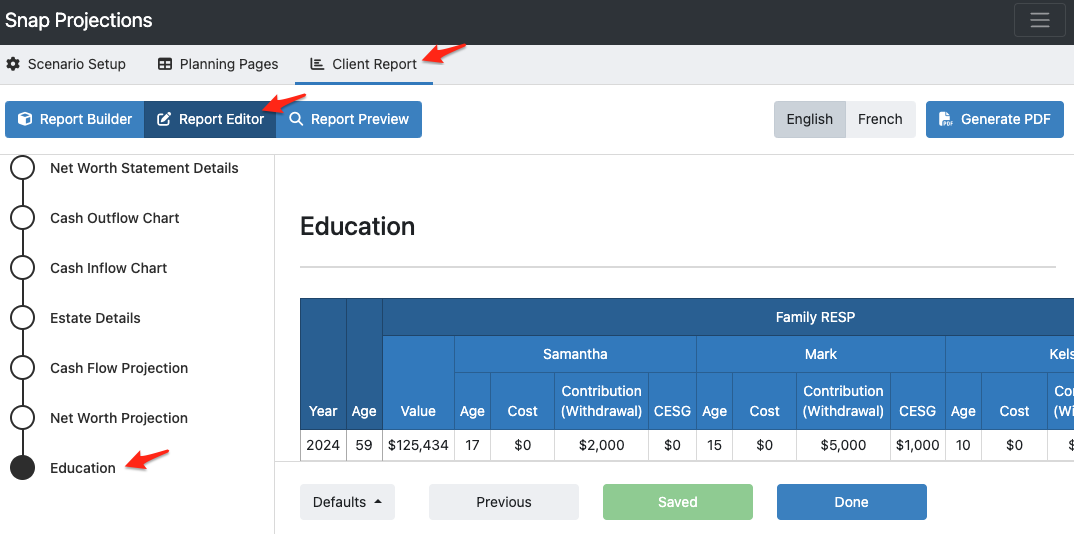

Viewing RESP in the Client Report.

Details about RESP as well as contributions/withdrawals appear in different areas of the client report. Click the images to enlarge them.

|

Education

|

|

|

Assumption Details

|

|

|

Cash Flow Projection

|

|