Charitable Donations: Insurance Donations

The following provides details on insurance donations specifically.

In this article:

- How to enter insurance donations

- Detailed examples:

- The donor owns the policy and designates the charity as the beneficiary.

- The charity is assigned as the owner of a new policy and as the beneficiary while the donor continues to pay the premium.

- The donor transfers the ownership of an existing policy in a specific year and continues to pay the premium.

- 1

-

How to enter donations from a Non-Registered Asset

Your client may choose to make a donation to a charity in the form of a life insurance policy. For all life insurance donation options, you will need to set the charity as the beneficiary for the policy.

|

|

|

|

|

|

If you don't see Charity as an option for the beneficiary, first enable charitable donations under Scenario Setup -> Settings.

- 2

-

Detailed Examples

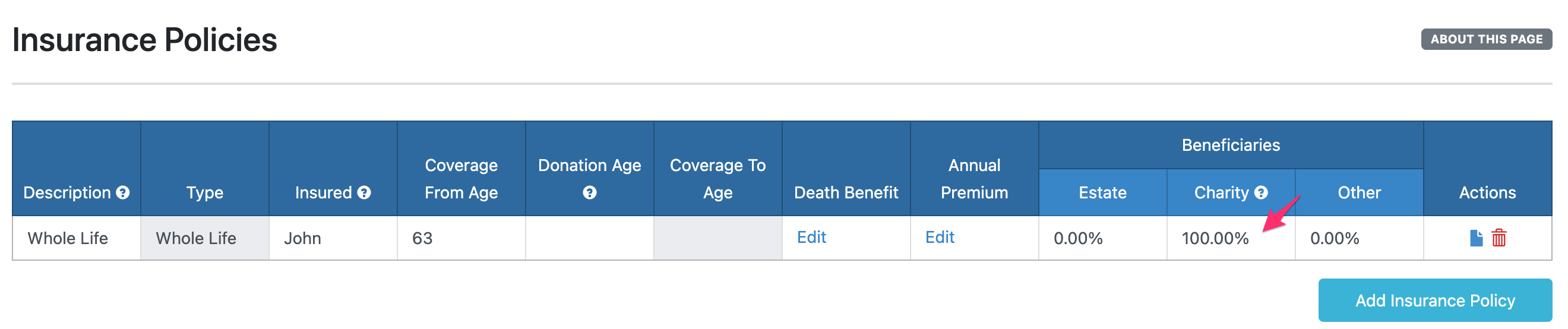

a. The donor owns the policy and designates the charity as the beneficiary

John owns a Whole Life Policy starting from age 63, for which a charity is designated as the beneficiary. In this case, the premiums paid by John do not qualify for a donation tax credit. The tax credit is applied upon the donor's death, when the charity receives the death benefit.

- Enter the policy in Scenario Setup -> Insurance -> Insurance Policies and designate Charity as a 100% beneficiary.

- In the final year of the projections, you will see a donation for the amount of the death benefit:

b. The charity is assigned as the owner of a new policy and as the beneficiary while the donor continues to pay the premium.

John takes out a new Whole Life insurance policy at age 63 with the charity designated as the owner and sole beneficiary. He continues to pay the premium which will be considered as a charitable donation and eligible for the donation tax credit. The death benefit and CSV are not considered a charitable donation.

- Enter the policy in Scenario Setup -> Insurance -> Insurance Policies and designate Charity as a 100% beneficiary.

- Enter the Donation Age the same as the Coverage From Age to assign the ownership of the policy to charity.

- All insurance premiums are considered to be charitable donations and will appear under the Premium column of the Charitable Donations section in the Planning Page table:

c. The donor transfers the ownership of an existing policy in a specific year and continues to pay the premium.

John owns a Whole Life policy from age 63 with his children as the beneficiaries. He donates the policy to charity at age 75 and continues to pay the premium. In this case, the CSV at the time of the transfer of policy will be considered to be a charitable donation that year. All insurance premiums that are paid by the donor will be considered a donation after the transfer of ownership. If the policy is fully paid up by that point, then only the CSV will be considered to be the donation.

- Enter the policy in Scenario Setup -> Insurance -> Insurance Policies and designate Other as a 100% beneficiary. This will ensure that the children receive the Death Benefit in the event of John's untimely death.

- Enter the Donation Age different from Coverage From Age to transfer the ownership of the policy to charity in the future.

- All insurance premiums are considered to be charitable donations and will appear under the Premium column of the Charitable Donations section in the Planning Page table. CSV will appear as a donation in the year the policy is transferred to Charity.