Charitable Donations: Overview

You can plan for cash, assets, and insurance donations and apply the associated tax credit to your projections.

The following steps illustrate how to set up the charitable donations and go into more detail on how the donations affect your projections.

In this article:

- 1

-

Enable Charitable Donations

|

|

|

|

|

|

- 2

-

Enter the Charitable Donations on the Planning page

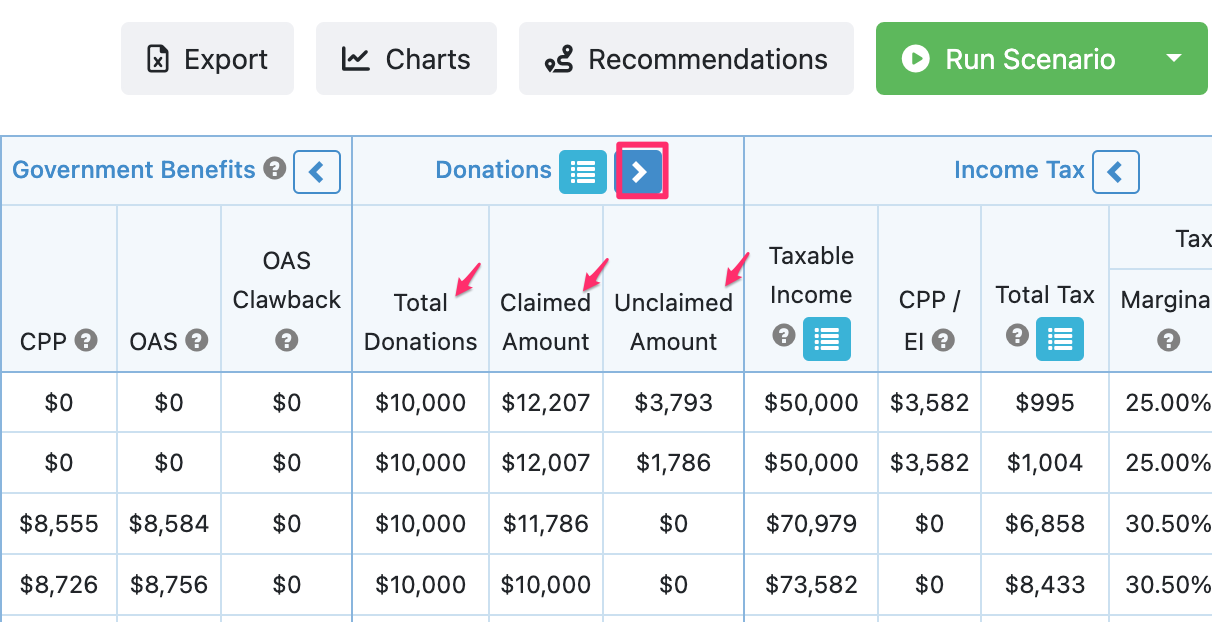

The Charitable Donations columns appear in between the Government Benefits section and the Income Tax section on the Planning page. By default, this section is expanded on the Individual Planning pages and collapsed on the Combined Planning page.

| Expanded View |

|

|---|---|

| Collapsed View |

|

In the collapsed view, the Total Donations column shows the total amount from all possible sources, cash, assets or insurance.

The Claimed Amount column shows the amount that is being claimed for tax purposes each year. Note that this amount will be the minimum of the following:

- total donations

- 75% of taxable income (or 100% of taxable income + estate tax in their final year)

- just enough to zero out either the federal or provincial tax.

The Unclaimed Amount column shows the total unclaimed amount being carried forward from previous years. Note that any unclaimed amount can be carried forward for 5 years. If there are unclaimed amounts to be claimed, Snap will always claim the ones with the closest expiration date first (i.e. with $6,000 expiring in 2025, and $5,176 expiring in 2030, Snap will deplete the 2025 amounts first before dipping into the 2030 amount.)

| If you hover your mouse cursor on top of the value in the Unclaimed Amount column you will see details on when the unclaimed amounts will expire. |

|

Please refer to these links for more information on the various types of donations: cash donations, donations from non-registered assets, and insurance policy donations.

- 3

-

View the Charitable Donations Details

|

From the individual's Planning page, click the blue menu icon in the header of the Charitable Donations section.

|

|

| To export this table to Excel, you can click the Excel icon beside the name of the table. |

|

Claimed Amounts

This section provides information about the claimed amounts for the client's taxes. For scenarios with a spouse, you will see two columns - for claimed amounts associated with donations made by the client and their spouse, where applicable. (See example below for more details).

Charitable Donation Tax Credit

Under this section, you can see the federal, provincial and total tax credits generated based on the donation amount being claimed. Keep in mind that this table is generated per spouse.

Total Tax

This section shows the taxes paid each year for this person and also displays what the taxes would have been if the donation was not made.

Example: Scenario with a Spouse.

In this example, John makes annual cash donations but his spouse, Jane, doesn't.

| John's Charitable Donations Details table |

|

|---|---|

| Jane's Charitable Donations Details table |

|

John's table (above) provides information about the claimed amounts for his taxes. He is able to claim donations that he made (From John) and no donations that Jane made (From Jane).

On Jane's Charitable Donations table, you can see the amount of donations that she claims for her taxes. She is claiming donations that John made since he would have no additional benefit if he made the claim himself (From John). She claims some of John's donations when it makes sense to do so. You can see how much tax she would have paid without claiming these donations in last column.

You will know for which spouse the table has been generated by looking on the first name listed under the Claimed Amounts section.

- 5

-

Charitable Donations in the Client Report

| Cash Donations |

|

|---|---|

| Donations from a Non-Registered Asset |

|

| Insurance Donations |

|

- 6

-

The Final Year of the Projections

In the final projection year, the client can claim up to 100% of their taxable income. The software will display a claimed amount that will bring federal and provincial taxes to $0.

In this final year, the total income used for cash donation purposes is the taxable income (i.e. the income being generated via employment and/or other income and/or withdrawals from assets) plus the deemed disposition of the assets. In other words, for the final year of the projections, the total tax credit that is calculated is based on the total tax plus the estate tax.

If one spouse's projections end before the other spouse's projections there is currently no rollover of unclaimed amounts of cash donations to the surviving spouse.