First Home Savings Account (FHSA)

For clients saving towards a first home, the FHSA can provide significant benefits. You can model this account type in Snap to show your clients the advantages of the unique tax treatment for contributions to and qualifying withdrawals from this account.

Watch this 5-minute summary video of the FHSA in Snap.

In this article:

- 1

-

Entering a FHSA in your project

On the Scenario Setup -> Assets page, you can select FHSA in the Type column.

Clients can have multiple FHSAs, which share the same contribution room and account closure requirements.

- 2

-

Contribution room controls and settings

Use the FHSA tab to adjust the default settings that Snap uses to determine the available Contribution Room for the FHSA each year of the projection.

The lifetime maximum contribution is $40,000, with $8,000 earned each calendar year once eligible.

If the client didn't contribute the maximum in a previous year that they were eligible to do so, up to $8,000 can be carried forward and entered in the FHSA Carryforward Room field.

If the client has made contributions in previous years, you can input the total in the FHSA Lifetime Contributions field so that Snap can factor this into its calculations. You can view the assumed Contribution Room available each year of the projection by hovering your mouse cursor over the Contribution value for the FHSA on the Planning page.

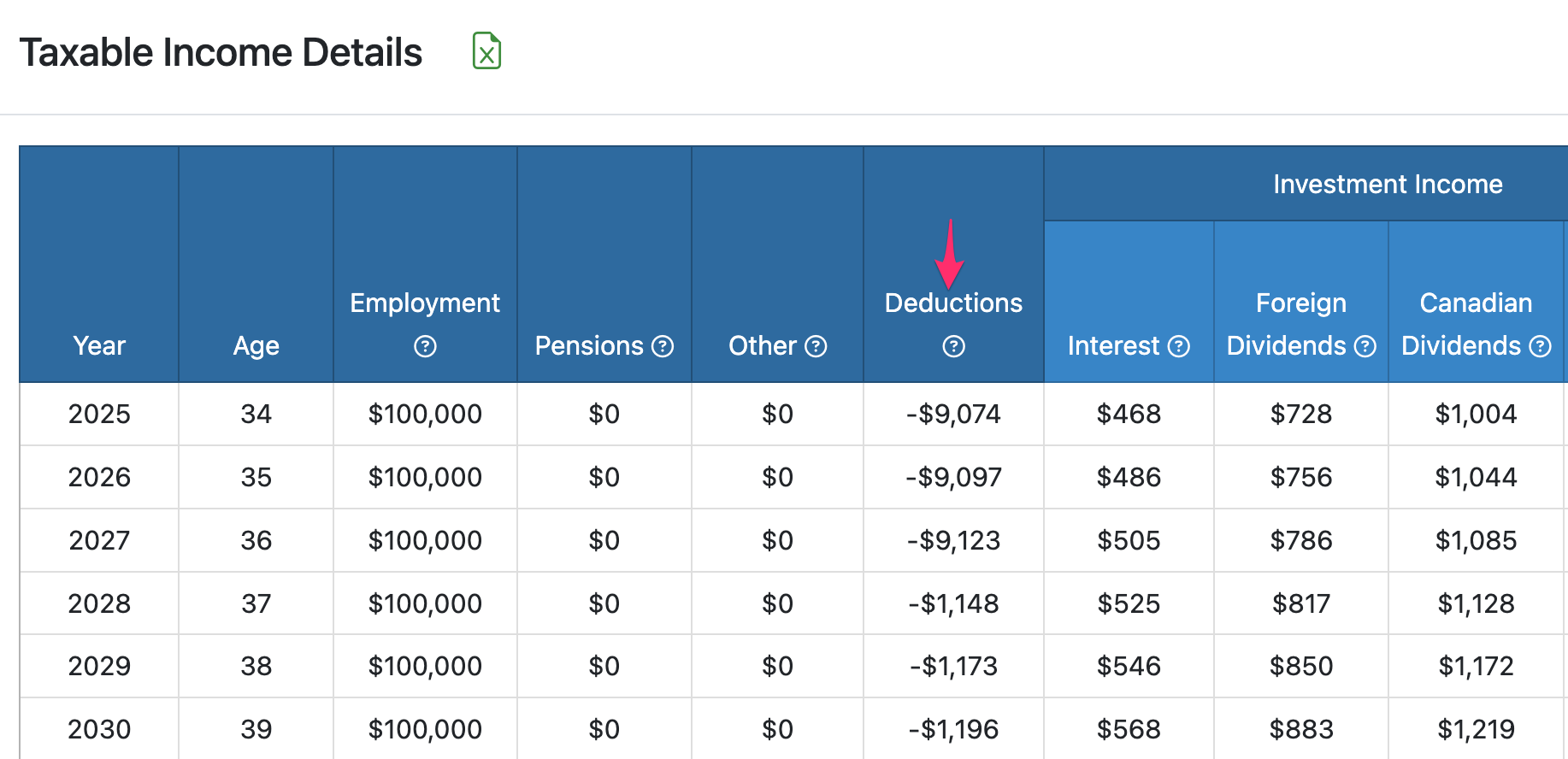

A Contribution to the FHSA can be used as a deduction against the client's Taxable Income for the year it's made. Snap automatically applies this Tax Deduction and displays the amount under the Taxable Income Details table available on the Planning page. The value contributed to the FHSA is reflected in the Deductions column as a negative value, reducing the Taxable Income.

- 3

-

Withdrawing money from the FHSA

The three primary ways that money can leave an FHSA are:

- The client can make a Qualifying Withdrawal when they purchase a qualifying property. This withdrawal is non-taxable.

- The client can make a Non-Qualifying Withdrawal at any time. This withdrawal is taxable to the client in the year it's withdrawn. The withdrawal does not increase the client's Contribution Room.

- The client can transfer the money to an RRSP/RRIF.

Qualifying Withdrawals

There are two ways that you can model a Qualifying Withdrawal in Snap.

If you're modelling the purchase of a first home in your projection, you can add the Real Asset with a Future Purchase Age and then select the Real Asset in the First Home dropdown on the Scenario Setup -> Assets -> FHSA tab. Snap will automatically make a Qualifying Withdrawal from the FHSA and apply it toward the cash flow required for the home purchase.

Alternatively, you can manually model a Qualifying Withdrawal by overriding the FHSA on the Planning page in any year of the projection (without requiring modelling the home purchase).

Because you can make a Contribution that reduces your Taxable Income and make a Qualifying Withdrawal that is non-taxable in the same year, the FHSA allows you to model contributions and withdrawals in the same year.

Non-Qualifying Withdrawals

If there is an FHSA balance in the year that the account is closed, Snap automatically distributes the remaining balance as a Non-Qualifying Withdrawal.

If you'd like to have this money flow to the RRSP, you can add the amount of the transfer to the client's existing RRSP Contribution Room on the Scenario Setup -> Assets -> RRSP/RRIF page so that the transfer does not impact the client's available room. You can use overrides on RRSP contributions on the Planning page to ensure this room is not used before the FHSA is closed.

Then, on the Planning page, you can enter a Contribution to the RRSP in the same year as the Non-Qualifying Withdrawal. The RRSP Contribution will offset the taxable income from the Non-Qualifying Withdrawal.

Transfer upon death

If there is an FHSA balance at the time of a client's death in a projection, Snap automatically transfers the balance to the surviving spouse's RRSP/RRIF.

- 4

-

Closing the FHSA

A client must close their FHSAs in the following three circumstances:

- The year after the client makes a Qualifying Withdrawal.

- The 15th anniversary of the client's first FHSA opening.

- The year that the client turns 71.

These closure requirements will reflect automatically in Snap. Any remaining balance at the time of an account closure will be taken as a Non-Qualifying Withdrawal.

You can adjust the assumption for the 15th anniversary by adjusting the First FHSA Opening Age field on the Scenario Setup -> Assets -> FHSA page.

- 5

-

Viewing the FHSA

The account value for the FHSA is included throughout the software (e.g., Planning pages, Client Report pages, Charts, Life Needs Analysis) as either a dedicated FHSA category or as a component of the Registered category.

For example, on the Planning page, the FHSA is displayed under the collapsed Financial Assets section.

Similarly, on the Cash Flow Summary pages of the Client Report, there is a dedicated column for the FHSA.

In other areas of the software such as the Net Worth Chart, the FHSA balance is added to the Registered category along with DCPP/LIRA/LIF and RRSP/RRIF balances.