Using Overrides

In this article:

- What are overrides?

- Baseline projections with no overrides

- Overriding default contribution amounts

- Overriding default withdrawal amounts

- Why the override value may change after running the scenario

- Using a $0 Override to force a contribution or withdrawal to/from the next available asset

- Overriding Income amounts

- Overriding the Amount Paid on a Debt

- 1

-

What are overrides?

The term override refers to a manual entry on the Planning page that changes the automatically generated value. Most commonly, overrides are used to make Contributions or Withdrawals for Financial Assets, but they can also be used to customize Income amounts, to change the Amount Paid to a Debt, and more.

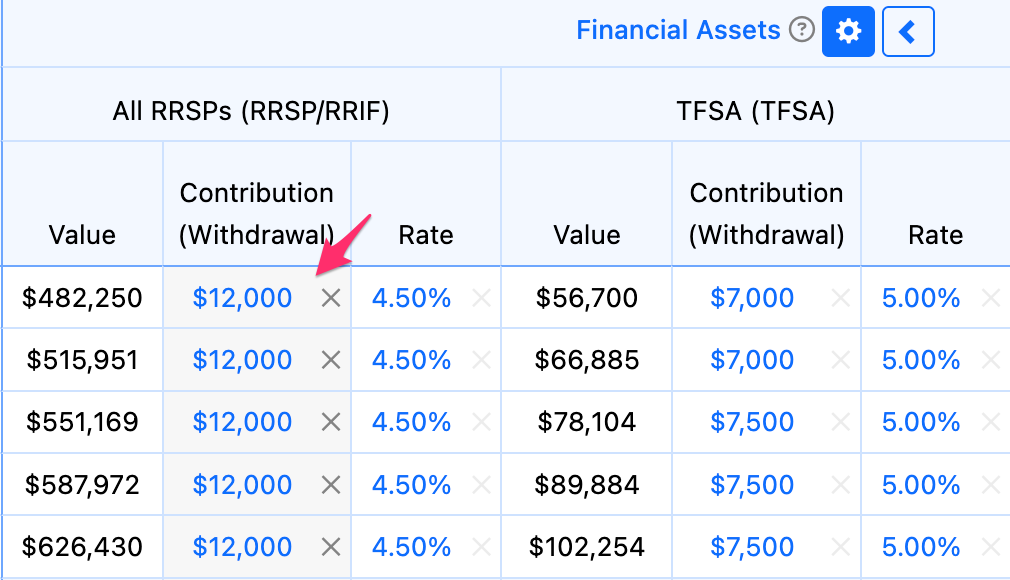

Overrides are evident by the highlighted background and the small "x" in the cell. This highlighting distinguishes the manual entries from the entries generated automatically by Snap. In the example below, a manual Contribution override of $12,000 is being made to the RRSP and the TFSA has automatic contributions.

Another option to change the automatically generated values in a projection is to adjust Scenario Settings.

- 2

-

Baseline projections with no overrides

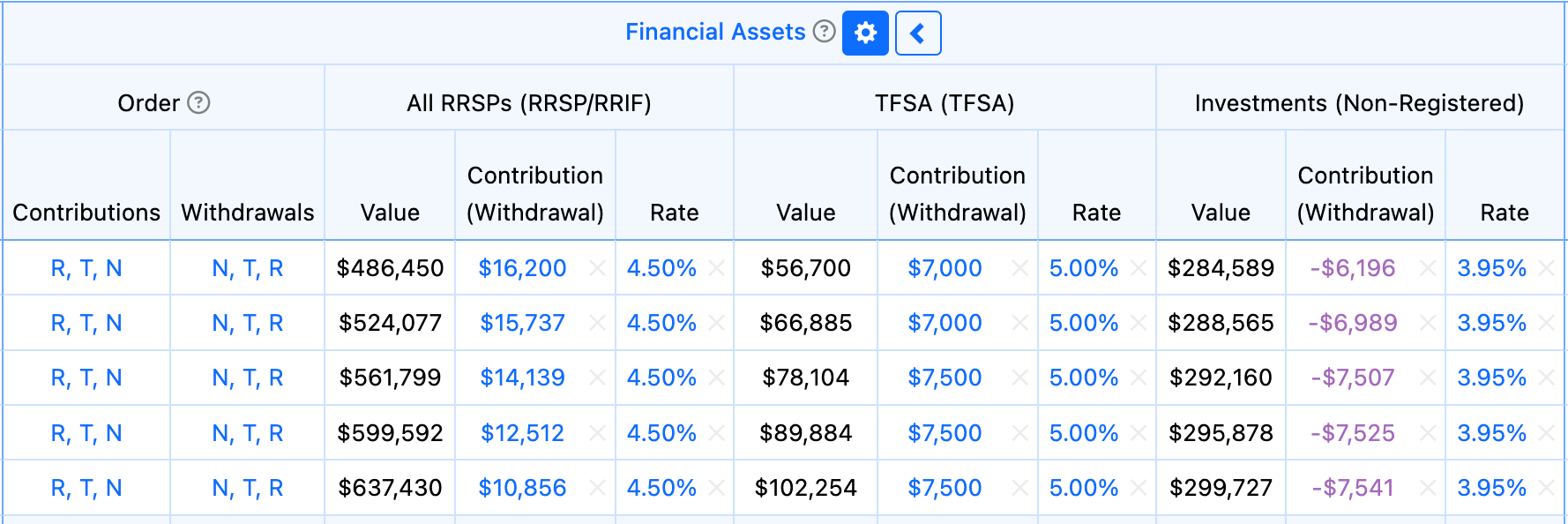

In this example, automatic Contributions are being allocated to the Financial Assets based on the default contribution order and the setting to automatically top-up the TFSA from the non-registered account. No overrides are present.

- 3

-

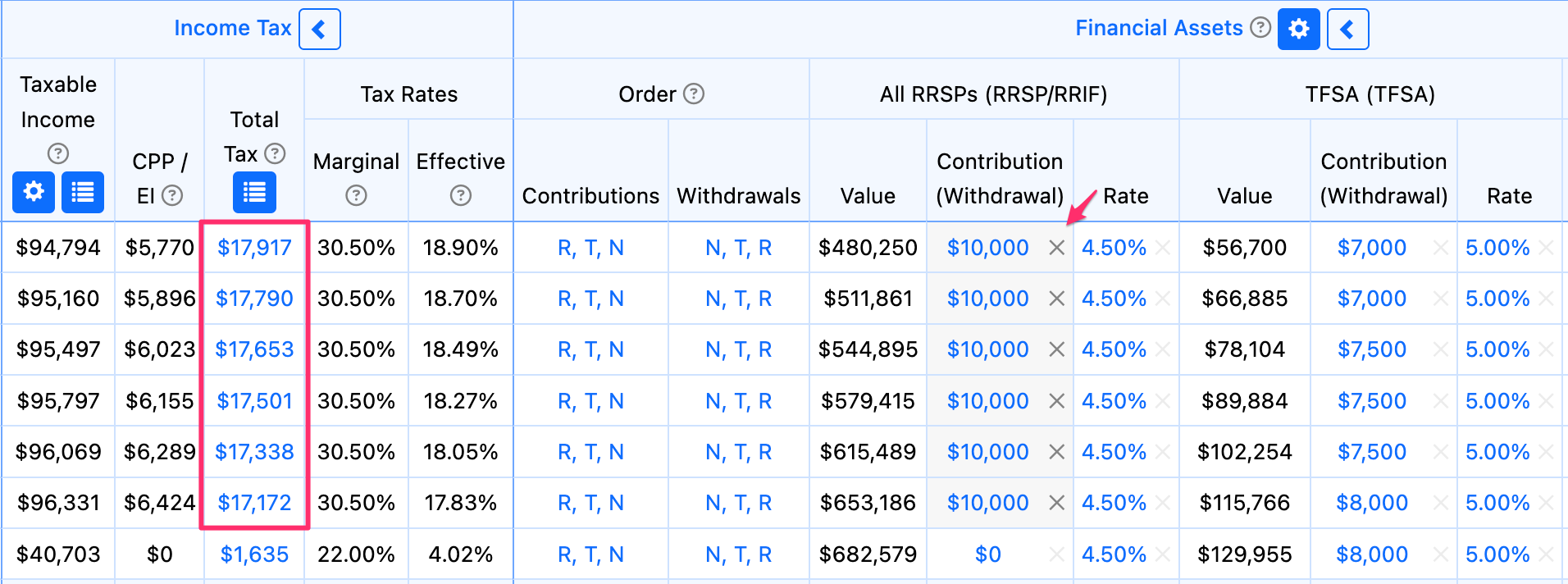

Overriding default contribution amounts

On the Individual Planning page (not Combined), make sure the Financial Assets section is expanded by clicking the right arrow icon in the section header.

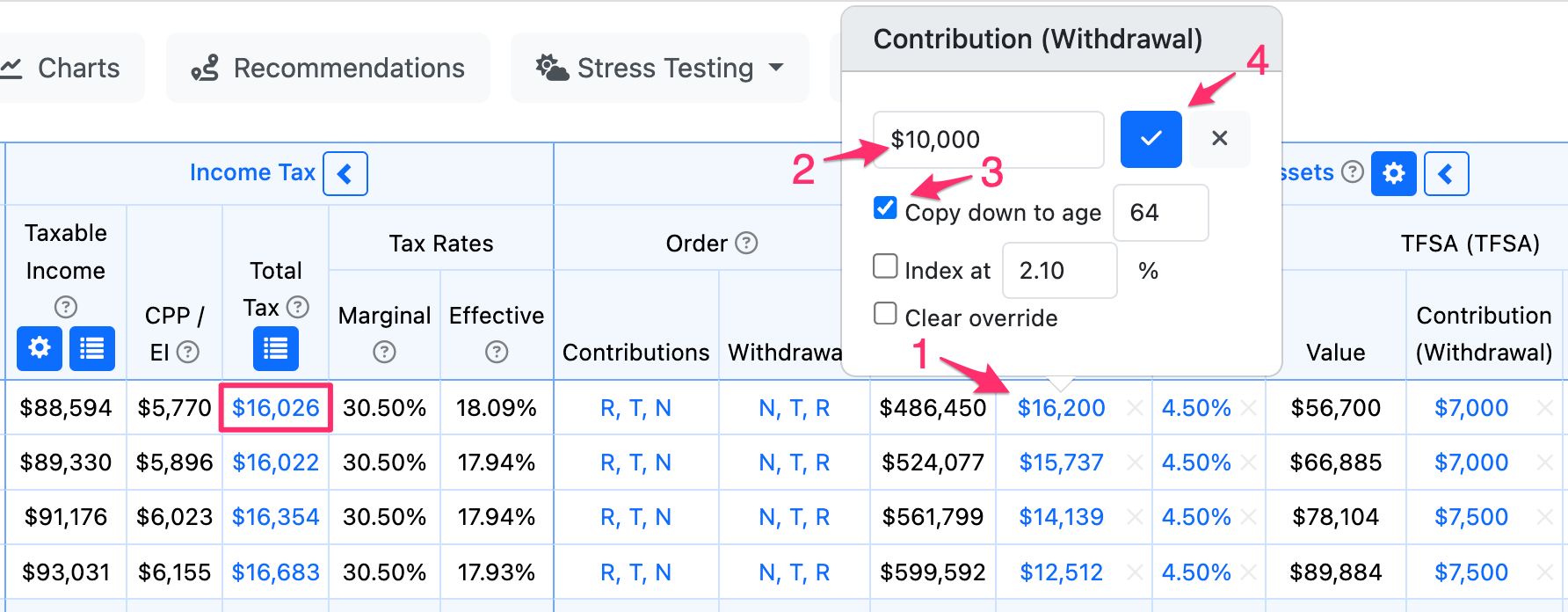

In the above example, the RRSP has a contribution of $16,200 in the first year. We can change this contribution to $10,000 as follows. Click the $16,200 amount in the Contribution column, enter $10,000 in the pop-up window, and copy it down until the desired age (64 years old in our case). To activate the entries, click the blue checkbox and Run the scenario.

After running the scenario, the $10,000 Contribution overrides to the RRSP are highlighted. The Total Tax is higher because the RRSP contributions are lower. Surplus cash is contributed to the other Financial Assets as specified under the Order section.

Contributions can be entered for all assets but remember that Snap will not make automatic contributions or withdrawals to the overridden accounts. This could create a surplus or shortfall which is tracked in the Cash Balance.

You can clear the overrides to revert to the automatic contributions and withdrawals.

To prevent automatic contributions to the Assets before retirement, move the CFM Start Age to the retirement year (the default setting).

- 4

-

Overriding default withdrawal amounts

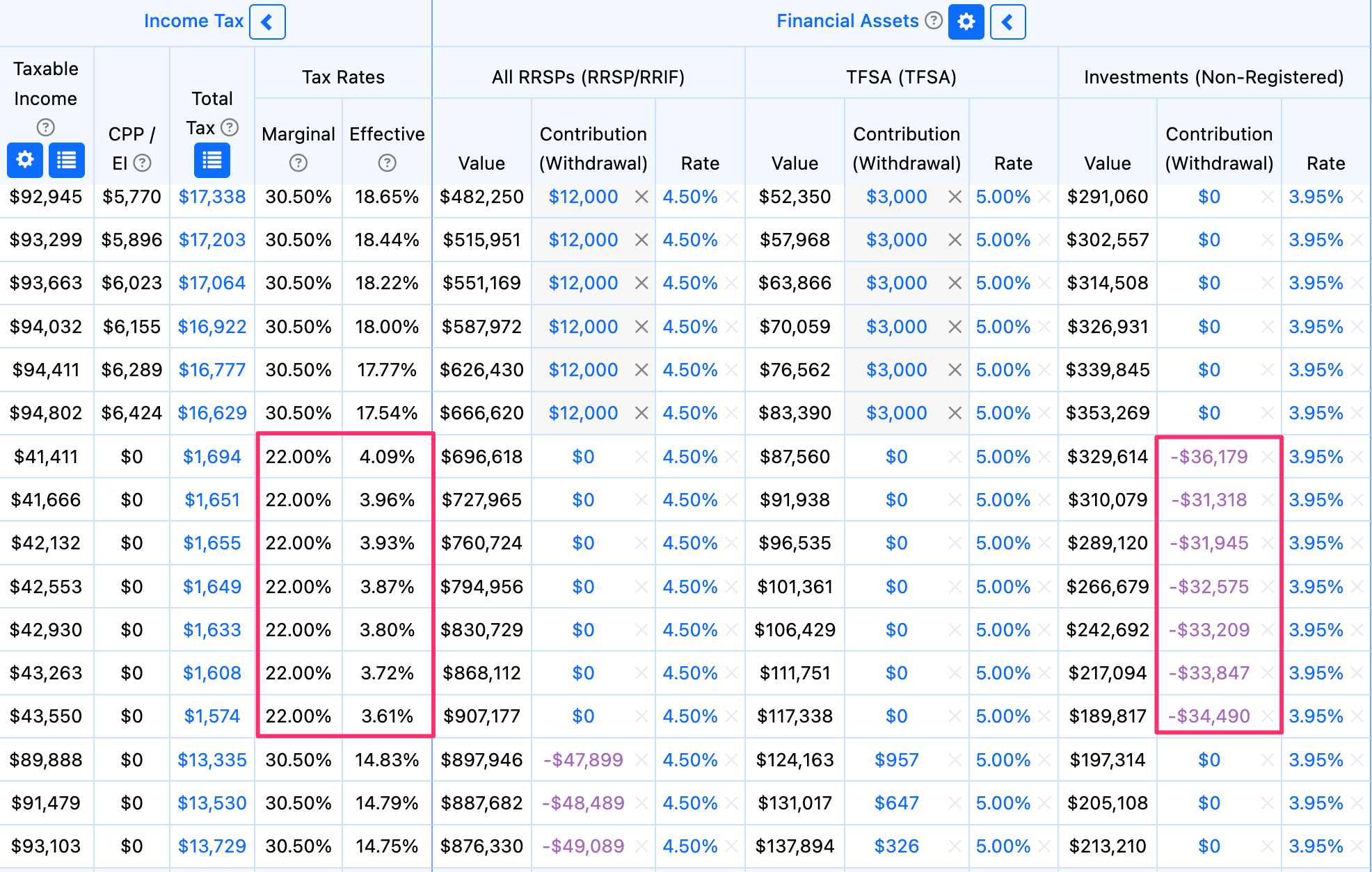

Withdrawal overrides are entered as a negative amount under the Contribution (Withdrawal) column.

In this example, the Base Expenses are funded solely by the Non-Registered account in retirement. The Tax Rates section on the Planning page can be used to see the Marginal and Effective tax rates each year. Until the RRIF minimum withdrawals commence, the client's Marginal and Effective tax rates are low. To even out the taxes, you can withdraw from the RRSP account using overrides. (Another method would be using the Taxable Income Targeting feature.)

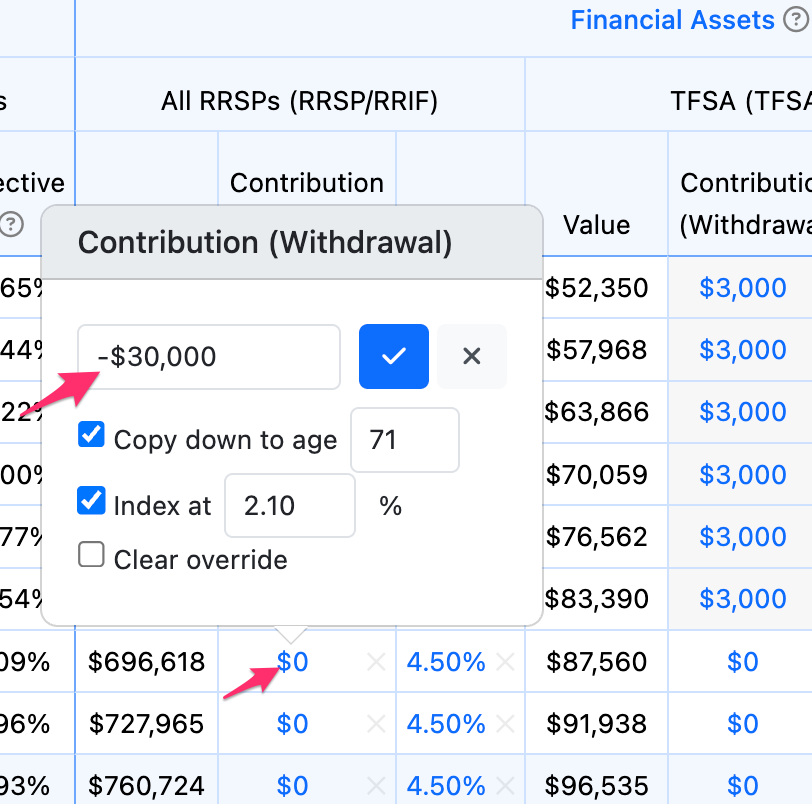

Click the $0 amount in the RRSP Contribution column in the year to start making withdrawals. In this example, let's set a withdrawal of $30,000 per year and index that at 2% each year. Since it is a withdrawal, you must enter a negative number for the Contribution(Withdrawal) column. Enter -$30,000 in the text box, click the checkbox to copy it down until the desired age (71 years old in this example), and click the blue checkmark.

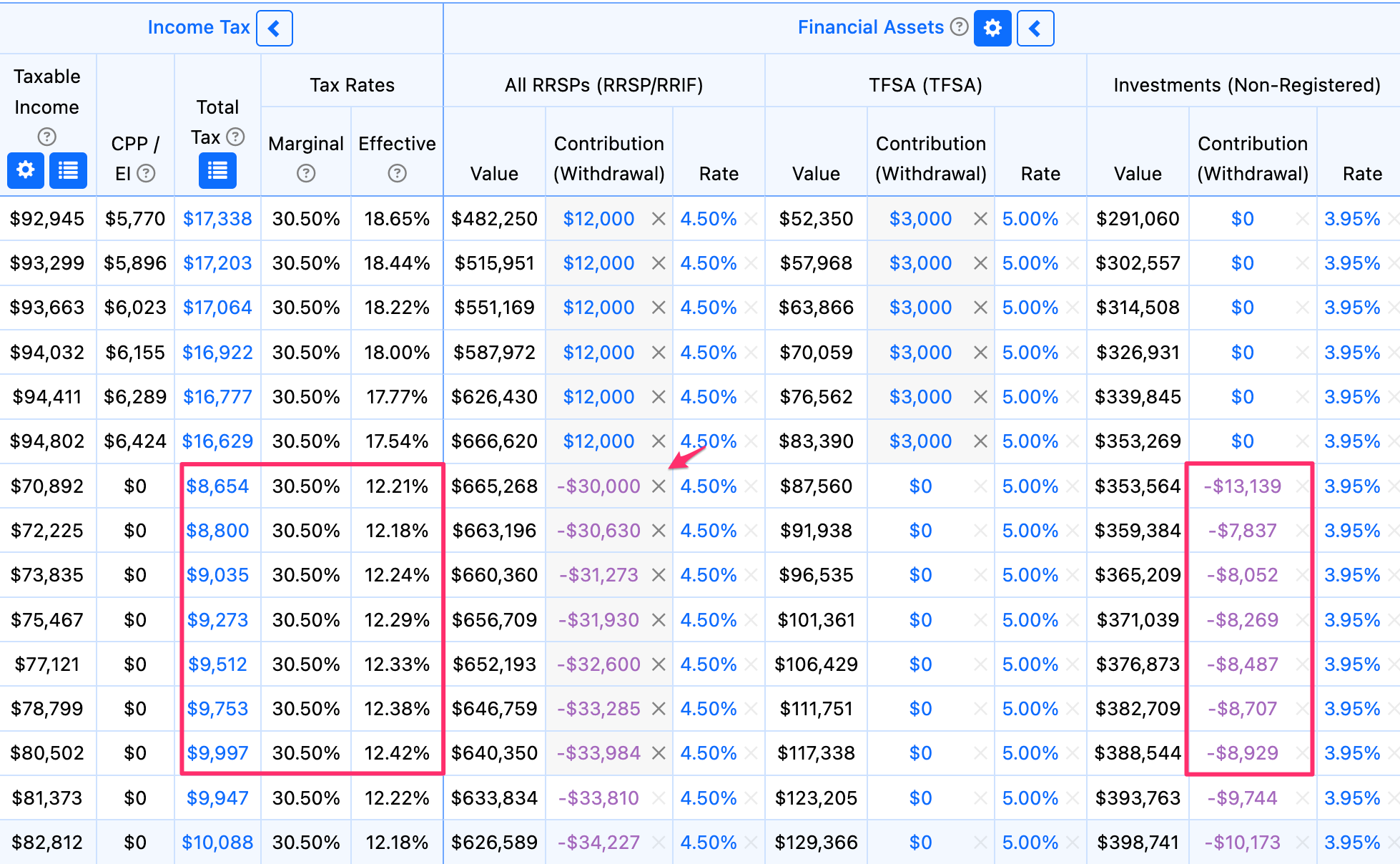

After running the scenario the updated projections are displayed.

Once the manual withdrawal from the RRSP is completed, if more income is required to meet the client's desired Base Expenses, the default CFM logic is used. Withdrawals are automatically taken from the Non-Registered account next. The client pays more in taxes over the years aged 65 to 71 than they did with no RRSP withdrawals, but they pay reduced taxes in later years because the required RRIF minimum withdrawals are now lower.

The automatic RRIF withdrawals start in the year the client turns 72. Snap will withdraw minimum RRIF withdrawals unless more income is needed based on the client's desired Base Expenses. You can use overrides to force minimum RRIF/LIF withdrawals or maximize LIF withdrawals.

In the above example, the client has a Non-Registered account that can be used to fund TFSA contributions each year. Snap Projections will not automatically withdraw more funds from the Non-Registered account to save to the TFSA, but you can also do this manually using overrides. You can also use overrides to maximize TFSA contributions.

Note: If you want to remove the overrides and let the software default to the specified logic, you can clear the overrides.

- 5

-

Why the override value may change after running the scenario

Snap will only accept an override value if it falls within acceptable parameters. In a case where entered values exceed required minimum or maximum withdrawals, once you run the scenario the value will be updated to fall within the limits. This is a helpful feature to maximize TFSA contributions, minimize RRIF/LIF withdrawals, and maximize LIF income.

Withdrawal value changes

If you want to force a specific RRSP withdrawal and the value entered is being automatically changed after running the scenario, please check:

- Did you enter the withdrawals as negative values (ex. -$2,000) to distinguish them from contributions?

- Does the software still consider this to be an RRSP account? Check the RRSP -> RRIF Conversion age.

Contribution value changes

If you want to force a specific RRSP/TFSA contribution and the value entered is being automatically changed after running the scenario, please check:

- Does Snap Projections know the first year's available Contribution Room?

- Has income been entered correctly? Confirm that all income entered under Scenario Setup -> Income has the appropriate setting for whether it is RRSP eligible. (RRSP eligible income will generate RRSP Contribution room during the projections.)

- Is there a Pension Adjustment (PA) entered? This will reduce RRSP Contribution Room each year. PAs should only be entered for DBPPs and not DCPPs.

- Has the RRSP been converted to a RRIF already?

- 6

-

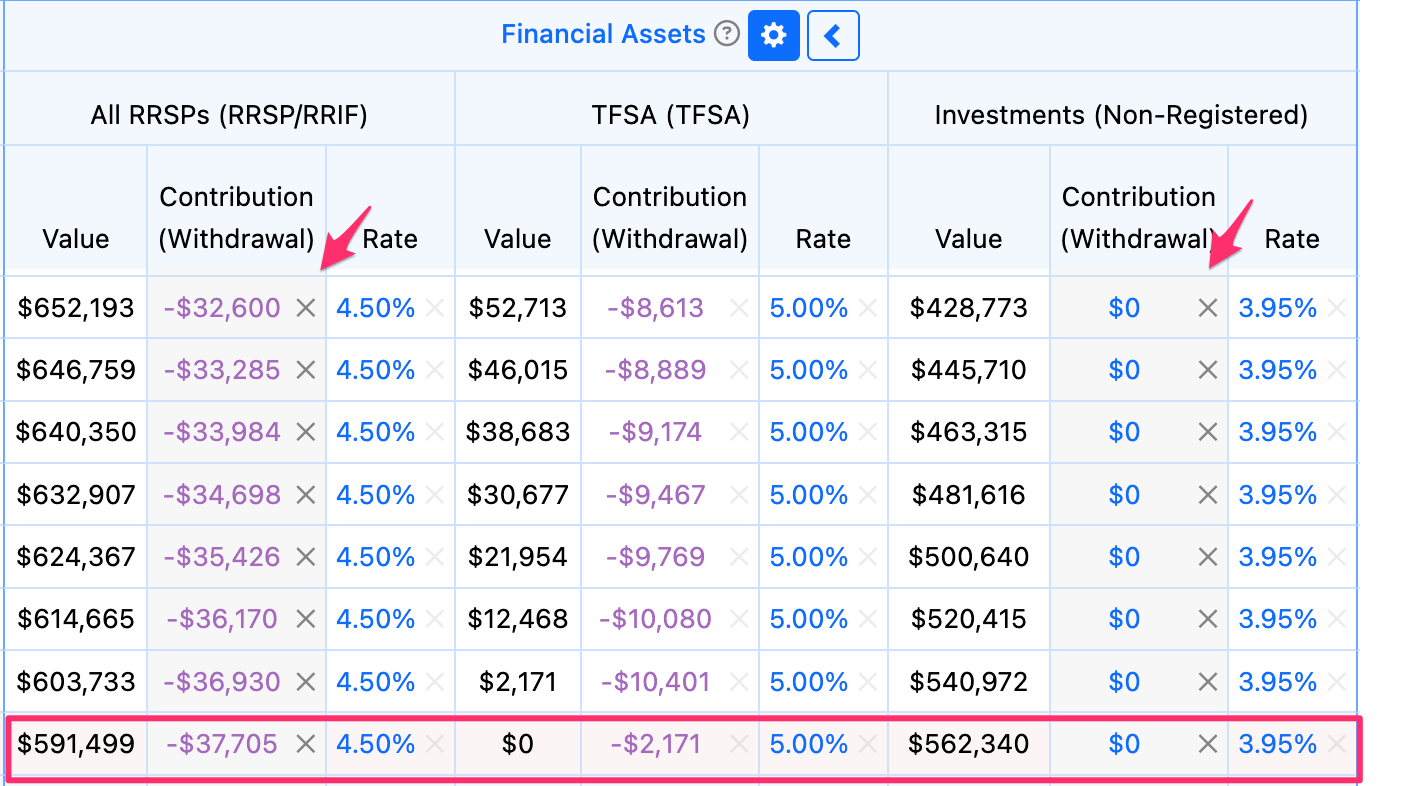

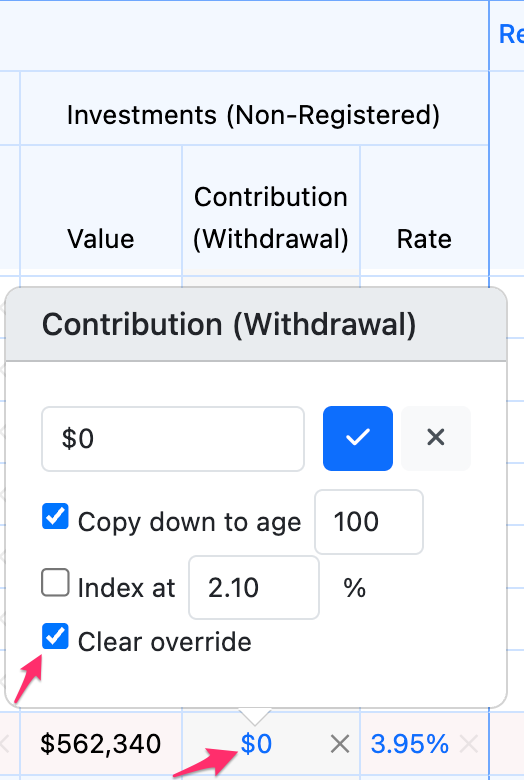

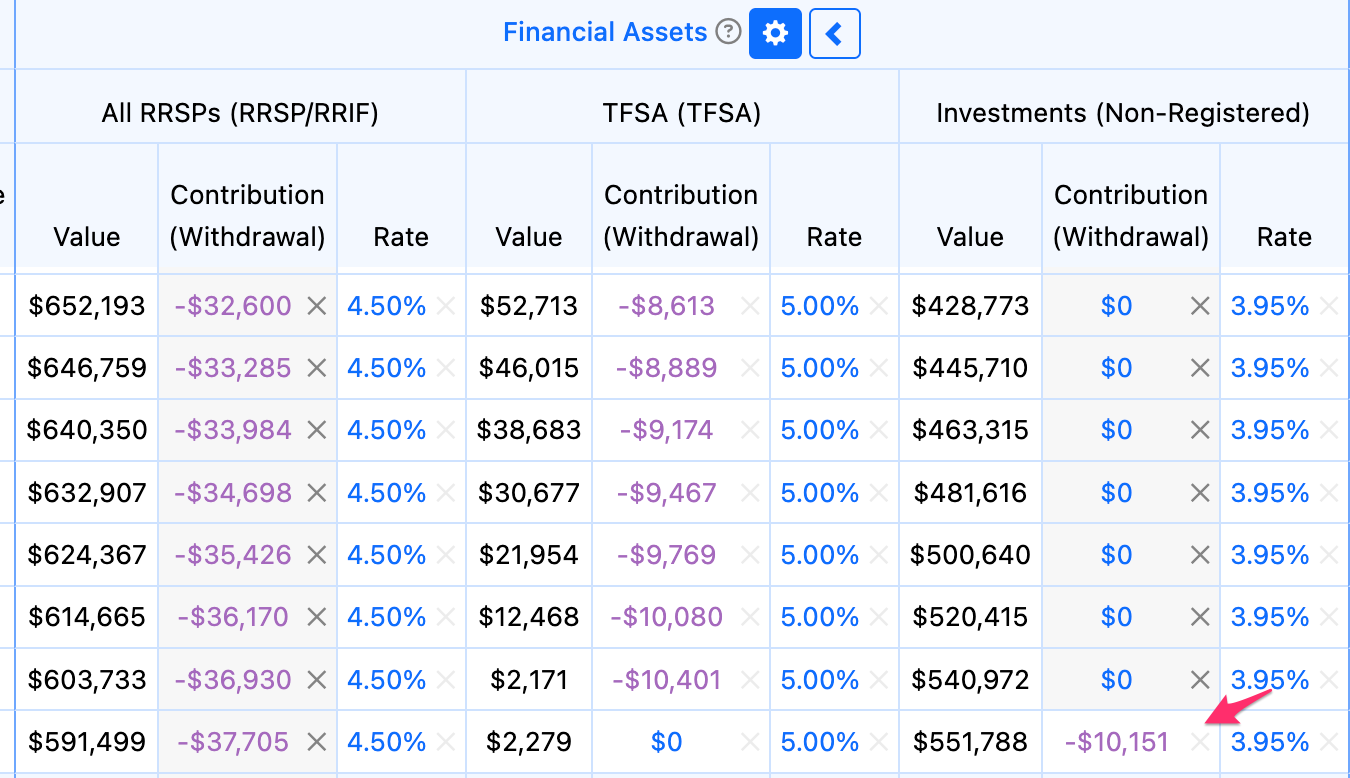

Using a $0 Override to force a contribution or withdrawal to/from the next available asset

If contributions are being made to an account that you don't wish to have contributed to, you can enter a $0 contribution override to prevent this. This will also work for withdrawals. For example, to prevent contributions to or withdrawals from the Non-Registered account in retirement, enter a $0 amount under the Contribution column for the applicable years.

Note the final year is highlighted in pink. This indicates a shortfall. By specifying the withdrawals from the Non-Registered account as $0 and the withdrawals from the RRSP as $27,738 in that year, there is not enough money in the remaining account (the TFSA) to cover the desired spending. The overrides prevent Snap from withdrawing more than what has been specified. To avoid the shortfall, clear the overrides on either the RRSP or Non-Registered account.

|

|

|

- 7

-

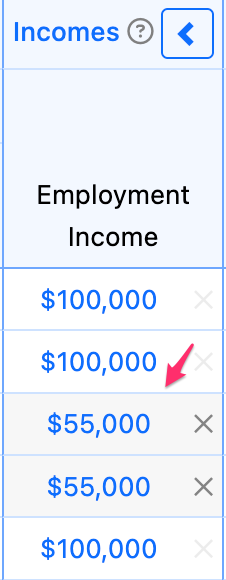

Overriding Income amounts

Once you've entered your desired Income sources on the Scenario Setup -> Income page, you can override values on the Planning page for individual years or periods.

For instance, if a client plans to work part-time for two years you can override the Employment Income on the Planning page to reflect this.

- 8

-

Overriding the Amount Paid on a Debt

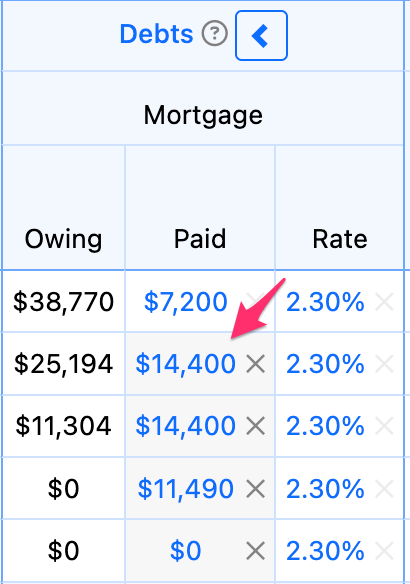

You can reflect accelerated Debt payments or new borrowing against a loan by entering overrides to the Amount Paid column of your Debt on the Planning Page. This is detailed further in Editing Annual Debt Payments on the Planning page.

Here we can model an accelerated mortgage payment starting in the second year of the projection by increasing the Amount Paid value on the Planning page by using an override.

A negative Amount Paid represents an amount borrowed rather than paid. This is helpful to model a line of credit.