January 20, 2026 - Release Notes - Enhanced Tax Transparency

| Summary: |

|---|

- New Features

We've released several new features to improve the tax transparency in Snap. These tools will allow you to see what's happening under the hood to better understand assumptions, calculations, and how different decisions will impact your clients' tax outcomes.

These changes are related to the clarity and detail provided in existing calculations. As a result, the tax values in your projections will not be impacted by this release.

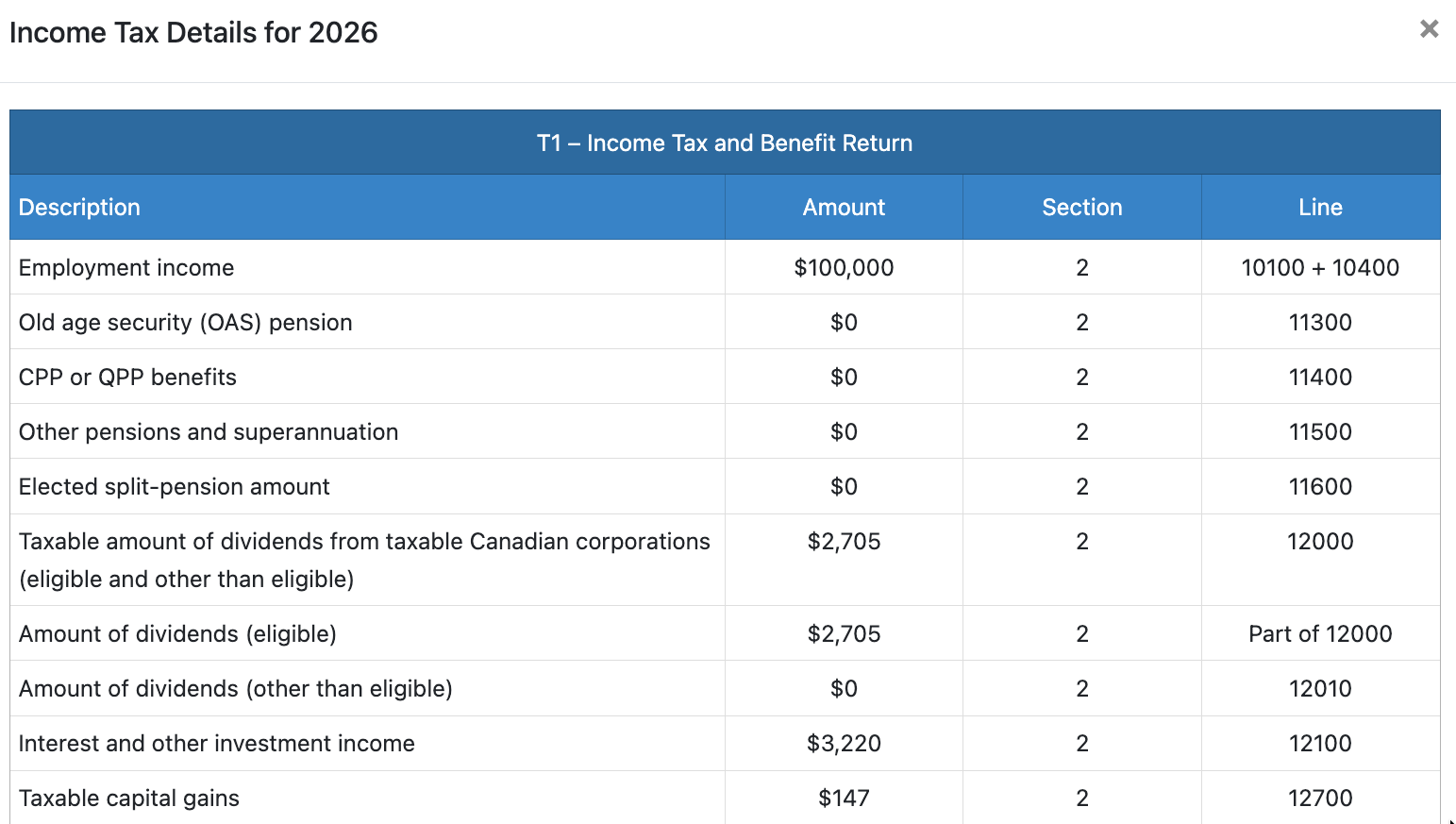

Personal Income Tax Details

You can now click on the individual Total Tax value in any year of the projection to access the Income Tax Details table. These values are provided on an individual basis and are accessible from the individual Planning Pages. You'll need to ensure that the Income Tax section is fully expanded.

The Income Tax Details table provides the income tax form fields used to calculate the client's annual taxes payable.

This table can help with understanding assumptions and calculations (e.g., that tax credits are indexed to inflation, the reduction to the age amount credit based on net income).

It can also help with illustrating the benefits of various strategies (e.g., partial conversions of RRSPs to access the pension tax credit, in-kind charitable donations).

Estate Taxable Income and Taxes Payable

New columns and tables have been added to the Balances section on the Planning Pages. You'll need to ensure that the Balances section is fully expanded to view them.

The Estate Taxable Income shows the total taxable income calculated in the final estate. This is on top of any Taxable Income realized in the calendar year included in the Income Tax section. These values are based on events in the estate, such as registered withdrawals, capital gains from deemed dispositions, and corporate distributions.

You can click on the box in the Estate Taxable Income column header to access the Estate Taxable Income Details table for a breakdown of sources. As a reminder, the Estate Taxable Income and Tax on Estate assumes no rollover of assets to a surviving spouse. This is for information purposes only and is designed to indicate the deferred tax liability on the Assets. If a spouse passes away in a projection, eligible assets are rolled over on a tax-deferred basis. More information on scenarios with a surviving spouse can be found in our dedicated article.

Definitions for each column are available from the (?) icon.

The Tax on Estate column now has a Tax on Estate Details table accessible from the box in the column header.

The Recovery Tax corresponds to any OAS received in the calendar year that would be clawed back in the final estate.

- Enhancements

Withdrawals from RRSP/RRIF accounts starting at age 65 are now considered pension income. This will result in the client receiving the pension tax credit (if they didn't already have qualifying pension income) and being eligible for pension income splitting.

Previously, withdrawals from RRSP/RRIF accounts were only considered pension income starting in the year the account was fully converted to a RRIF (based on the Conversion Age on the Scenario Setup -> Assets-> RRSP/RRIF page).

In many cases, advisors will transfer small balances from an RRSP to a RRIF starting at age 65 to generate pension income for tax planning purposes. This previously required you to add a second RRSP/RRIF account in Snap to model some balances as RRSP and some as RRIF, starting at age 65. This approach is no longer required. Any withdrawals made from the RRSP/RRIF starting at age 65 will now be included in pension income in Snap.

As a result of this change, some of your projections will be impacted when you next access them.

If there are RRSP withdrawals between age 65 and the current RRSP/RRIF Conversion Age, your projection will be impacted since there will now be a pension credit applied to this income (if the client didn't already have other qualifying pension income during the period), and it will enable pension income splitting (if appropriate). These should both improve the client's projection (since they will create tax savings). However, due to potentially unique cases (e.g., differences in rates of return between spouses), there could be cases where this change reduces the projected estate of an existing scenario.

| Back to top |