After-Tax Savings

In this article:

- 1

-

Activating the Savings column

Savings automates Contributions(Withdrawals) before the CFM Start Age to allow you to compare different savings strategies and find the best approach for your client. This column is automatically enabled when you apply the Required/Available Savings or Lump Sum Recommendations to your projections.

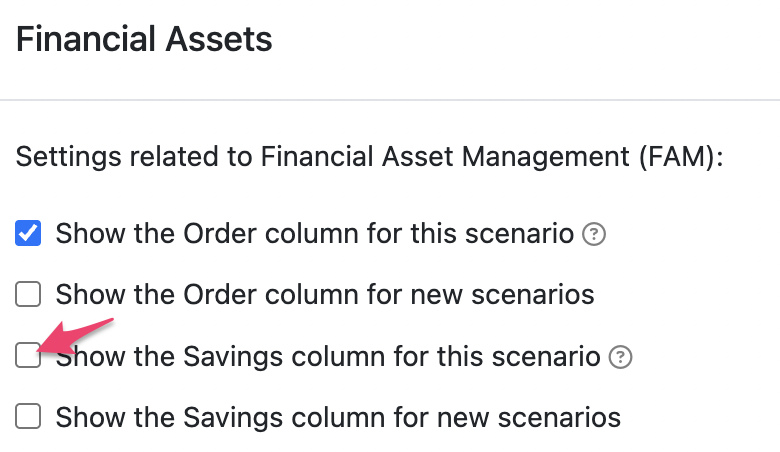

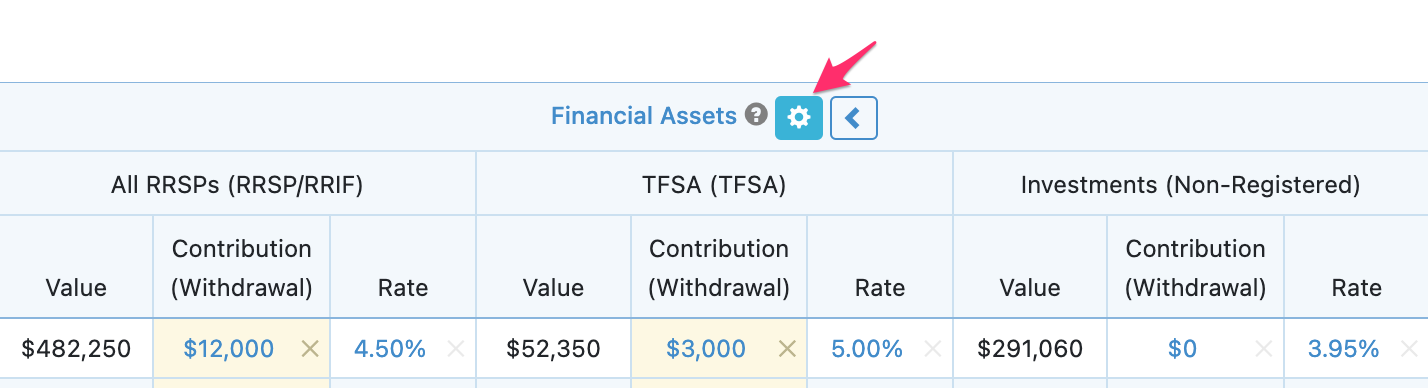

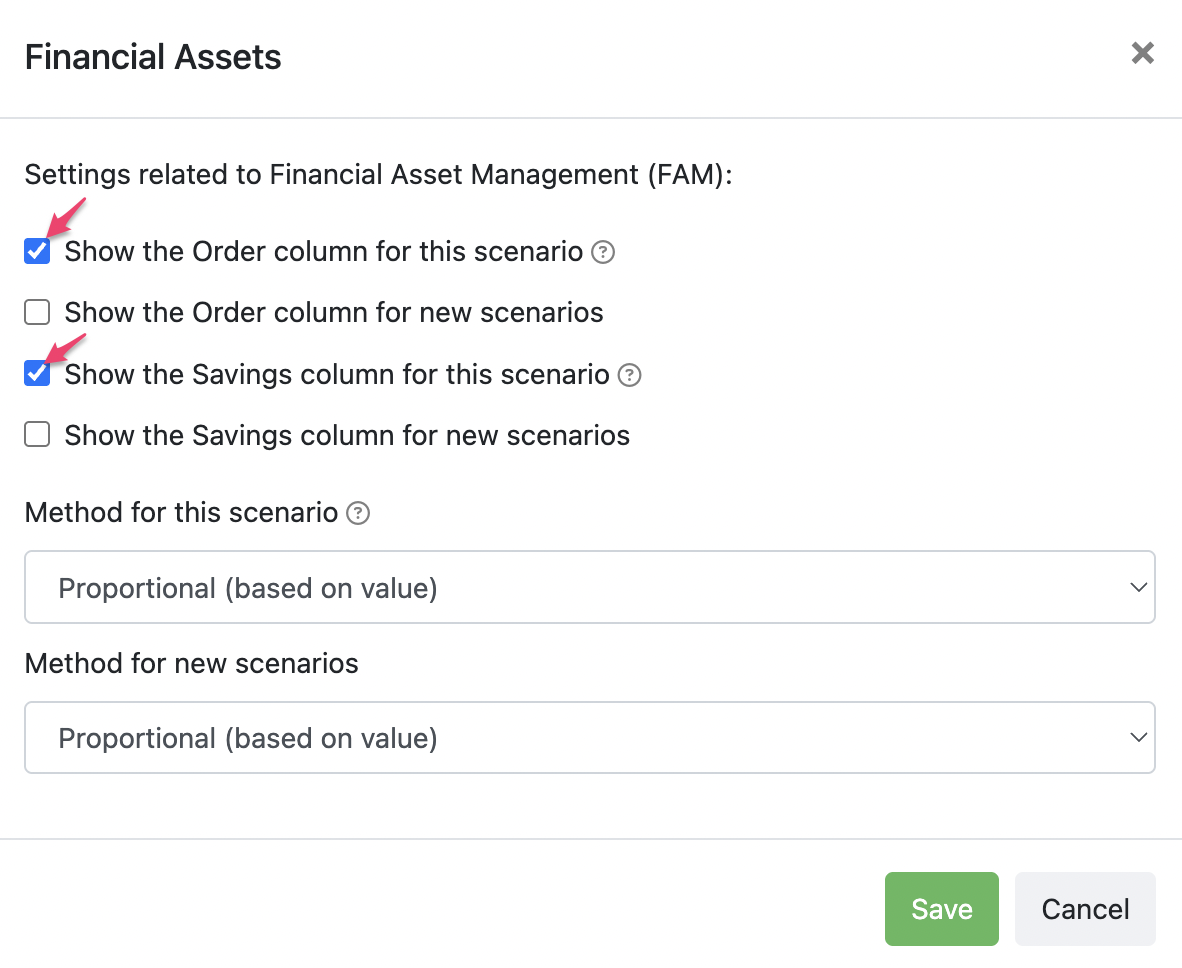

To activate the Savings feature manually, click the blue gear icon in the Financial Assets header of the Planning Page.

Then, check the box Show the Savings column for this scenario and Save. If you will use this feature regularly, check Show the Savings column for new scenarios.

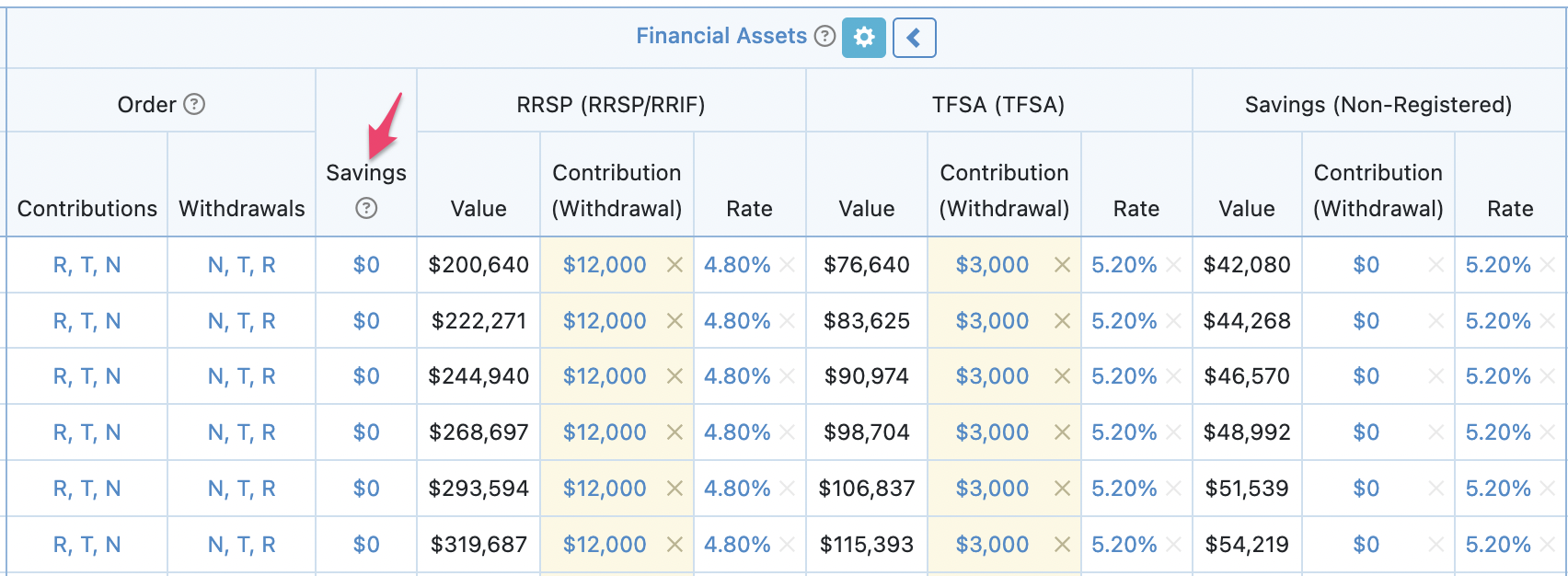

This creates a new column titled Savings on the Planning page.

The column allows you to set a target additional After-Tax Savings value for the years before the first Retirement Age or the CFM Start Age (whichever is earlier in the plan).

- 2

-

Using the Savings column for deposits

The Savings column allows you to enter a target additional after-tax savings amount for a given year or period. Snap will allocate automatic Contributions to the Financial Assets based on the Order.

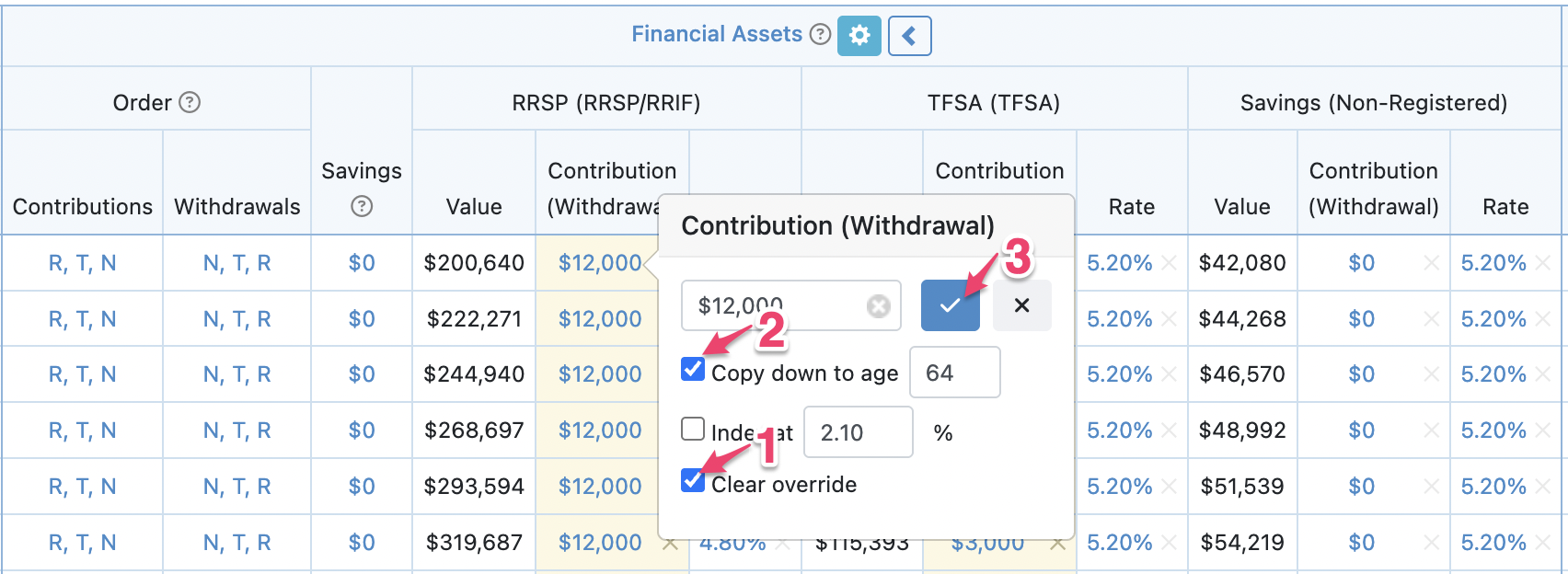

If there are any manually entered contributions or withdrawals, clear these overrides on the Financial Assets first and run the scenario. (See Using the Savings column with overrides if you don't want to clear the overrides.)

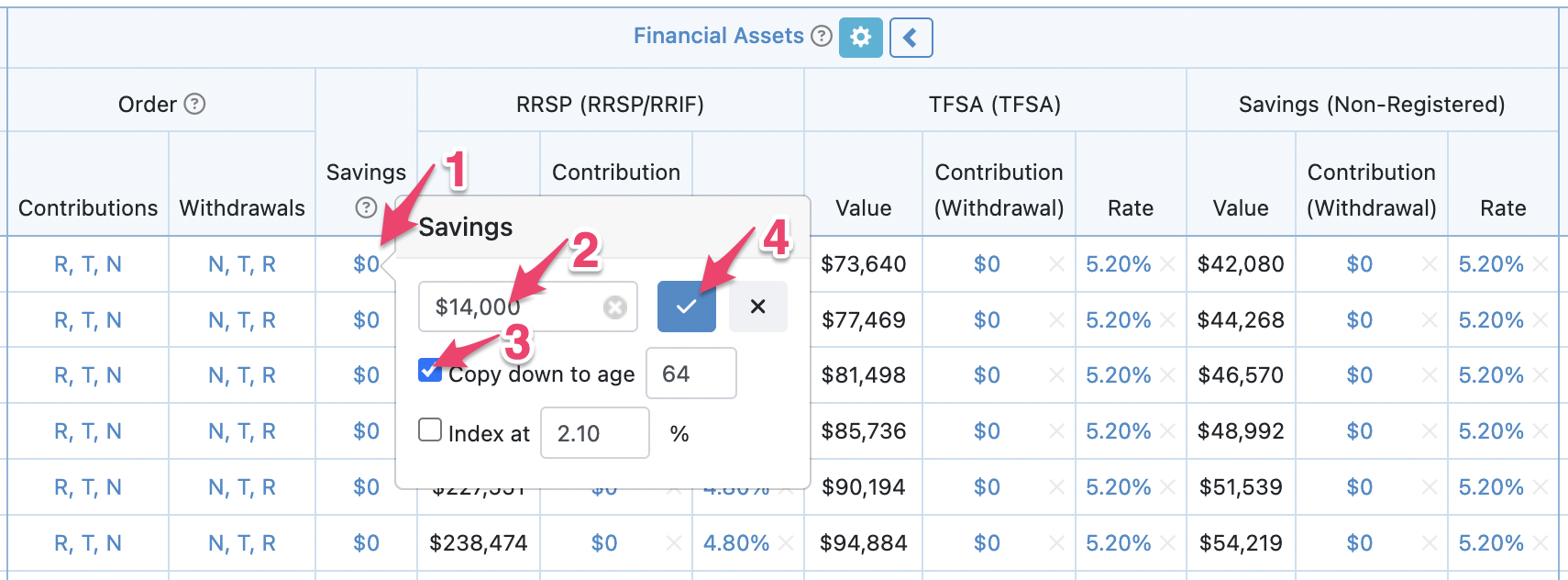

Enter the Savings value. In this example, we use a target after-tax savings of $14,000.

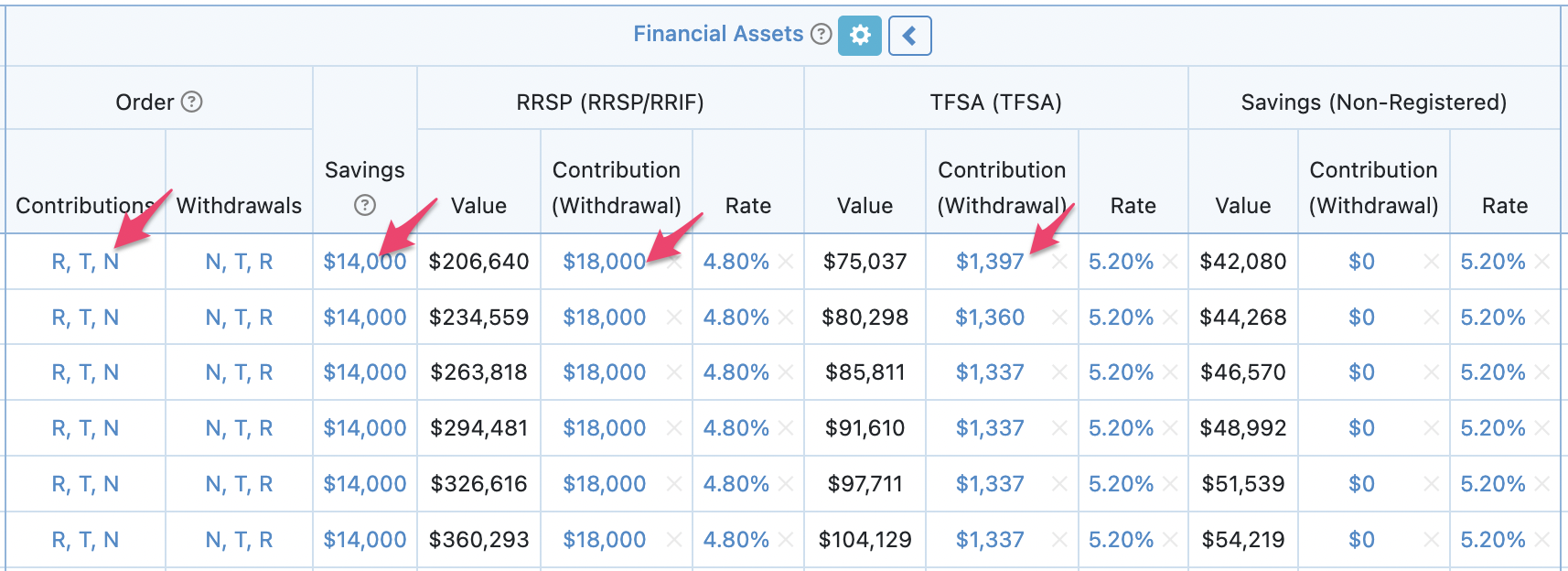

After running the scenario, the automatic contributions are visible.

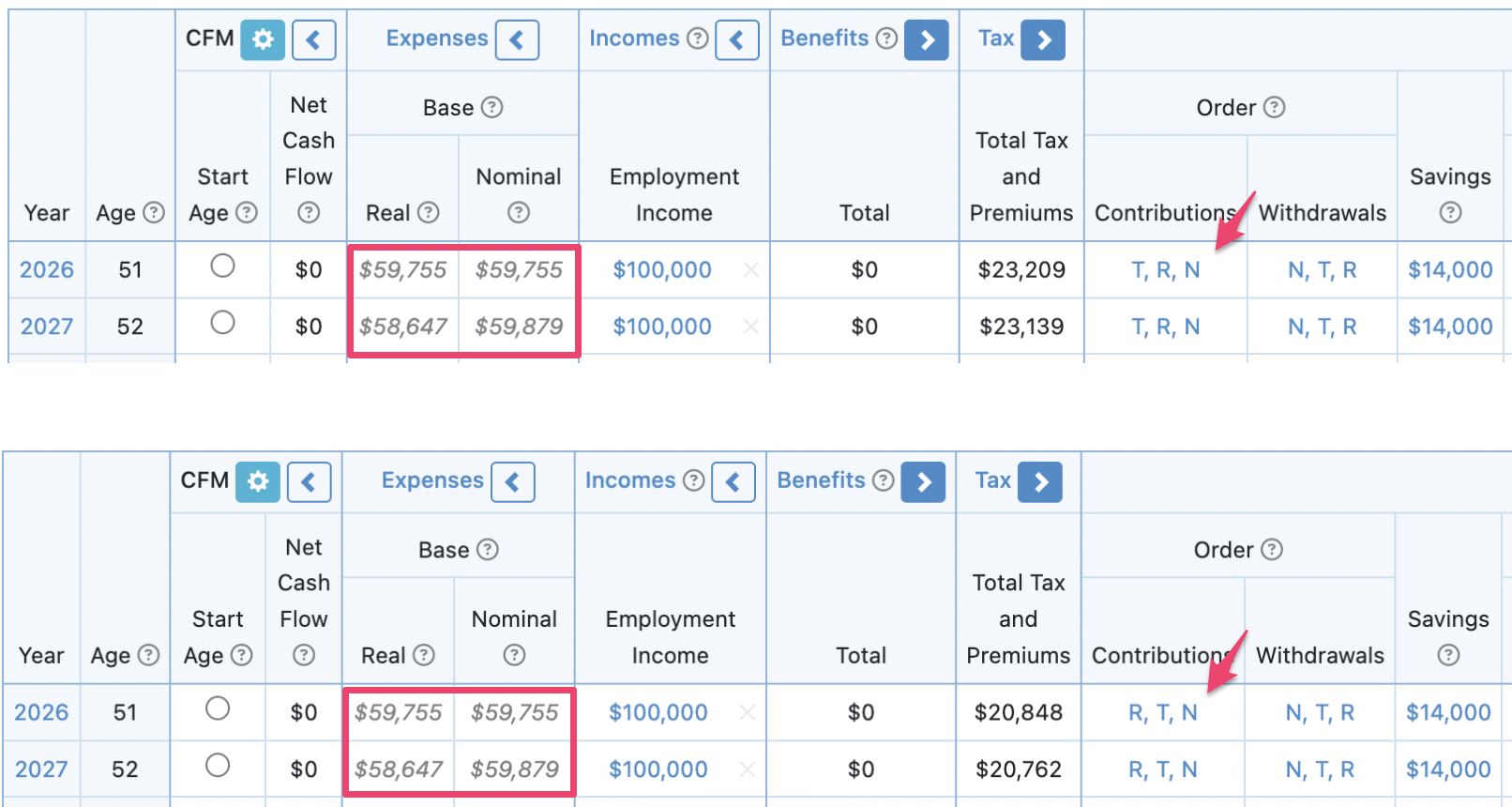

In this case, $18,000 is contributed to the RRSP (this is client's maximum RRSP contribution room) and $1,397 is contributed to the TFSA, based on the Order for Contributions, (R, T, N). The gross savings are $19,397 and the tax reduction of $5,397 from the RRSP contribution brings the total after-tax impact on cash flow to our target of $14,000.

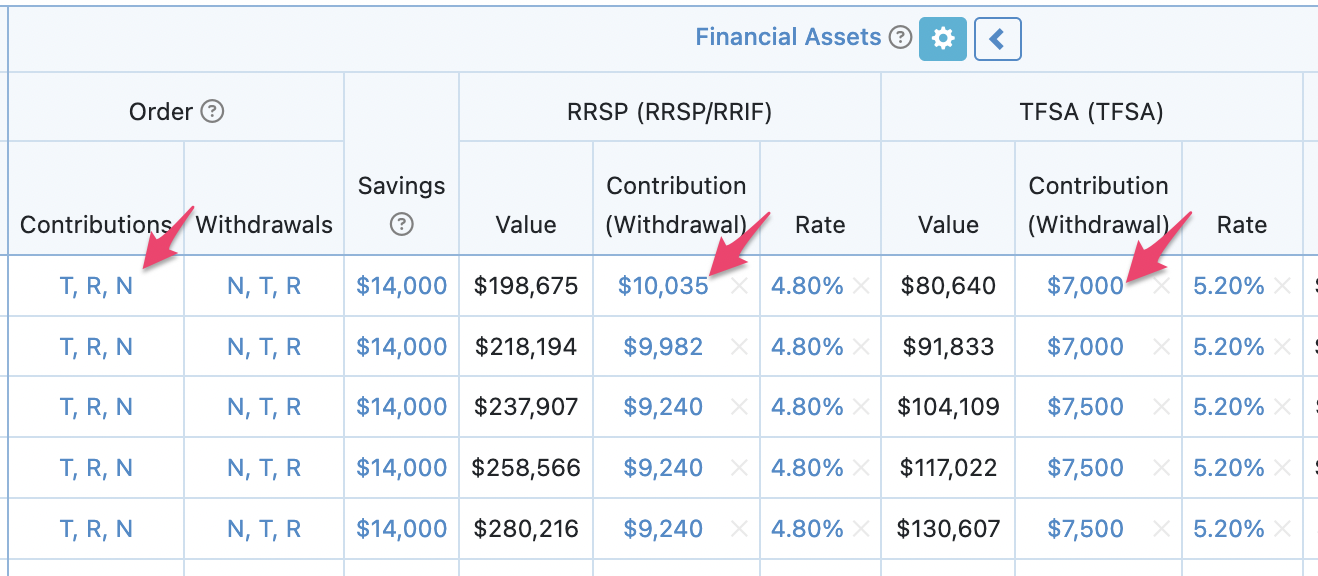

If we change the Order for Contributions to T, R, N, Snap will maximize the TFSA contributions first, then contribute the rest to the RRSP, achieving the same $14,000 of after-tax savings.

For this client in the first year of the projections, saving $10,035 to an RRSP and $7,000 to a TFSA is equivalent to saving $18,000 to the RRSP and $1,397 to the TFSA with respect to the after-tax cash remaining.

The Base Expense values in both scenarios are identical, meaning that the client is assumed to spend the same after-tax amount on their lifestyle, no matter if they have maximized RRSP contributions first, or TFSA contributions first. This allows you to compare the scenarios.

This feature can help you determine how much additional savings the client requires and where to make those Contributions.

- 3

-

Using the Savings column for withdrawals

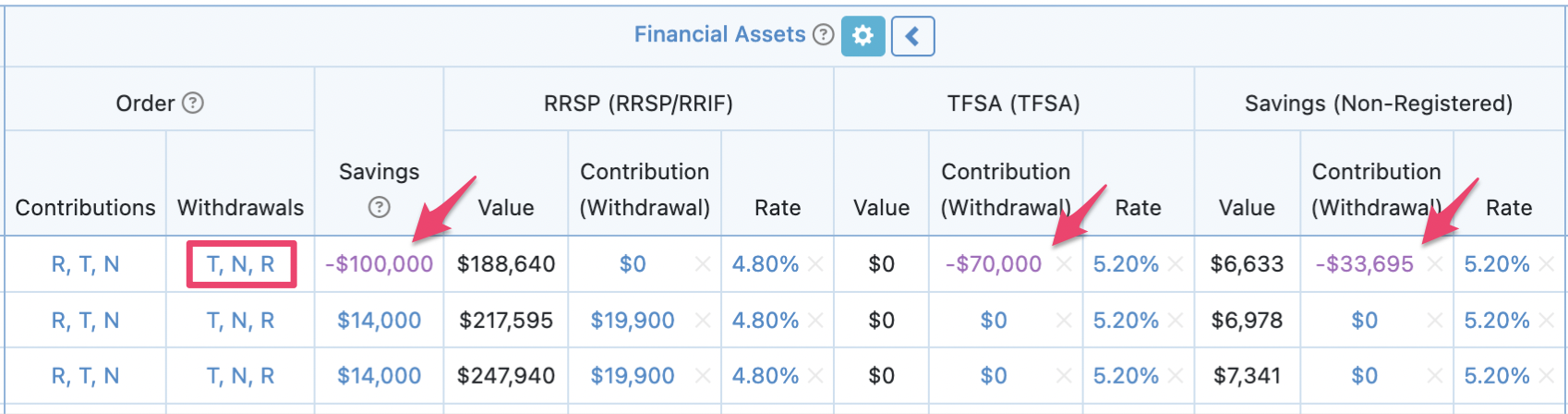

You can also use the Savings column to automate withdrawals. If you enter a negative value in the Savings column Snap will use the Order for withdrawals to achieve your target after-tax withdrawal value.

If a client requires $100,000 for a home renovation or gift, you can compare different withdrawal strategies to see which approach best meets their goal factoring in tax implications.

- 4

-

Using the Savings column without Financial Assets

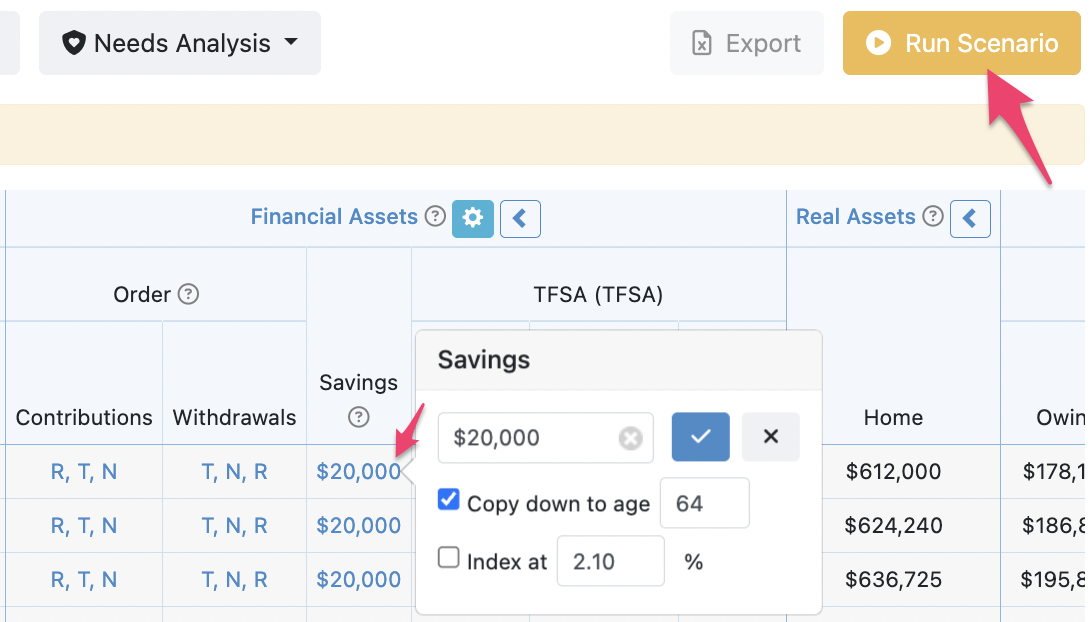

Savings relies on the the existing Financial Assets in the plan. If you enter a Savings value and then Run Scenario, the value entered may be reduced if there aren't available Financial Assets to contribute to.

For instance, if a client's TFSA Contribution Room is $7,000 and that is the only Financial Asset entered, the Savings maximum value is $7,000.

For example, enter $20,000 for Savings.

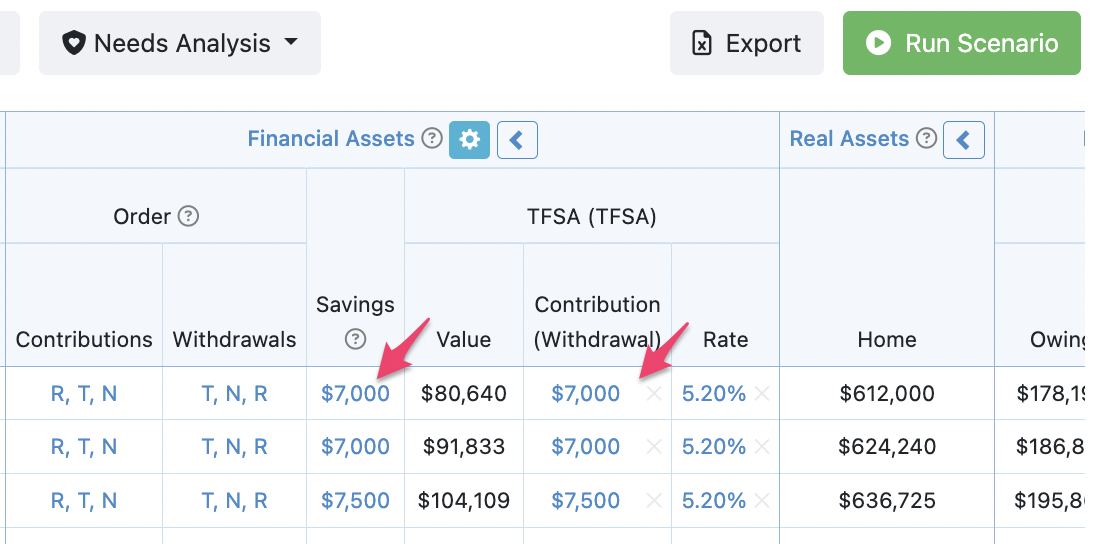

Click Run Scenario and Snap will change the Savings to $7,000.

As a result, it's recommended to have a TFSA, RRSP and non-registered Financial Assets entered into the plan before using the Savings column. If the client doesn't have one of the account types, you can enter it on the Assets page with a $0 Value.

If you have multiple accounts of the same type (for example, two non-registered accounts) then contributions to these non-registered assets will be proportional based on the value of the accounts. To change to a sequential order of contributions or withdrawals, adjust the Method.

- 5

-

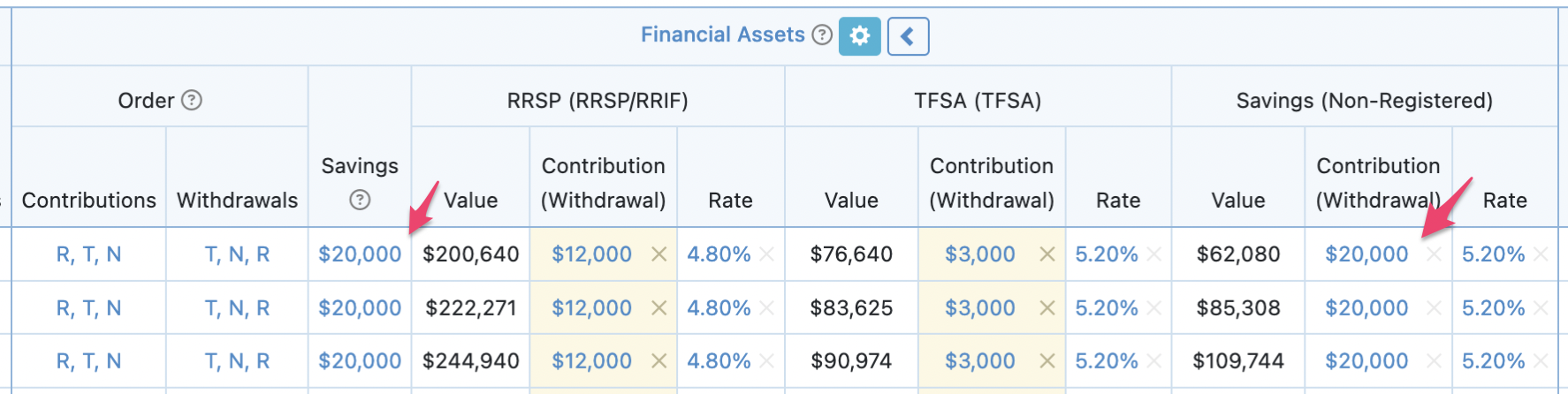

Using the Savings column with Overrides

It's common in Snap to use overrides to contribute to Financial Assets on an annual or ongoing basis. You can use the Savings column in addition to manual overrides but it's important to understand how the two pieces of functionality interact.

A value entered in the Savings column will be saved to the client's Financial Assets in addition to the contributions that you've overridden manually.

In this instance, the $20,000 of Savings is deposited to the non-registered account in addition to the $12,000 manually contributed to the RRSP and $3,000 to the TFSA. Since there are overrides on both of these accounts, the only available Financial Asset for deposits is the non-registered account.

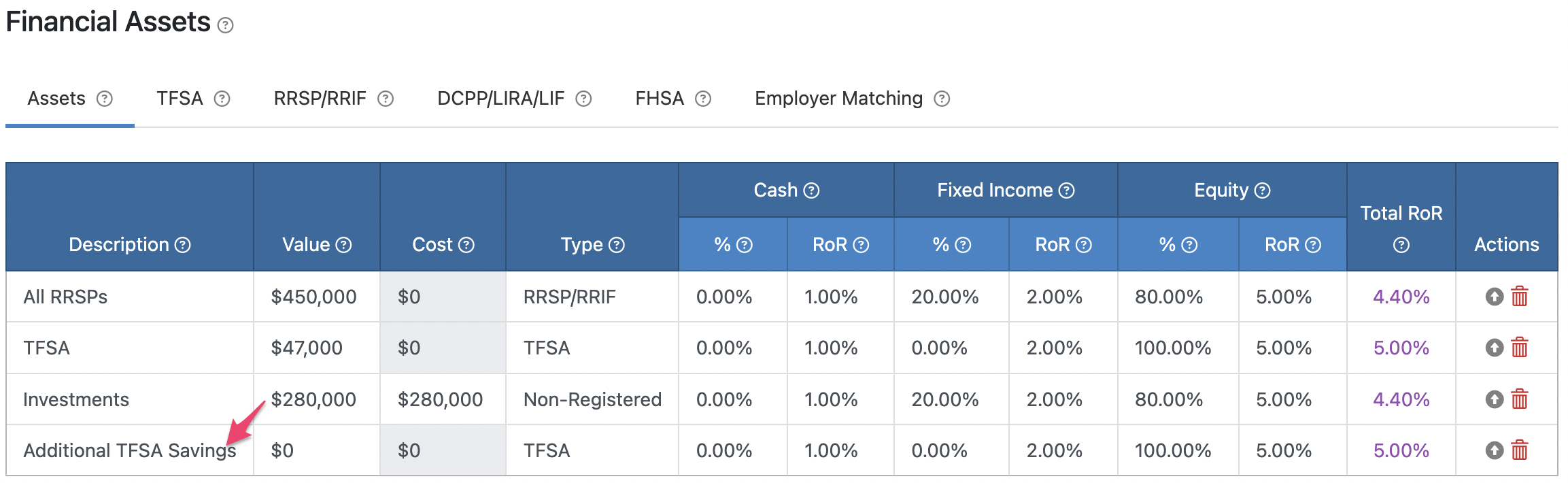

If you'd like Savings to be allocated to a TFSA on top of your manual overrides, you'll need to add a second TFSA to the plan with a $0 Value.

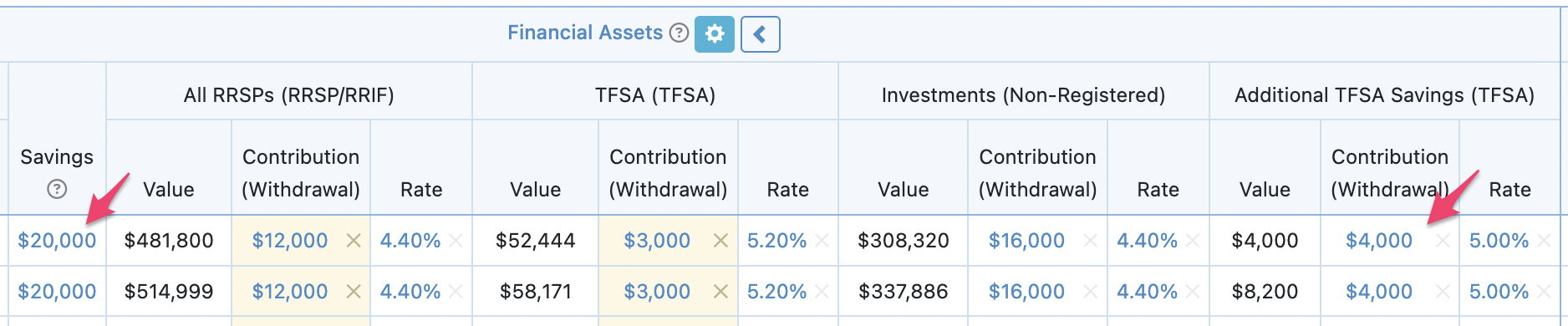

After adding the new TFSA, the Savings tool can allocate contributions to this account up to the available contribution room. Snap then deposits any remaining savings to the non-registered account.

- 6

-

Clearing the Savings column

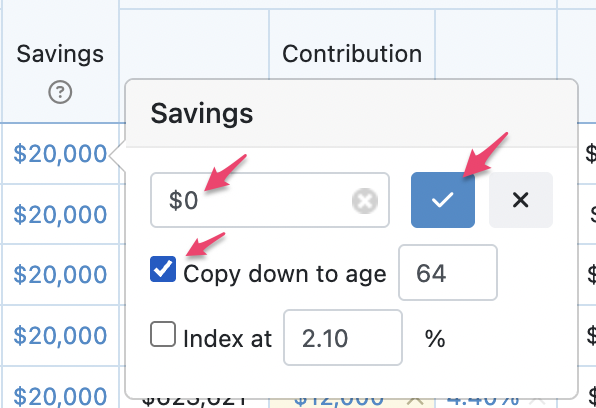

There are two primary ways to remove a previous Savings amount.

1. You can select the dollar value and change it to $0 (for a given year or period).

2. You can turn off the Savings column within the plan to set all values to $0. Then if you want to continue using the tool you can turn it back on to set new savings values.