Cash Flow

In this article:

- 1

-

Overview

The easiest way to understand the cash flow in Snap Projections is to think about it as the cash left after paying taxes and deductions, expenses, investment contributions, debt payments, insurance premiums, and charitable donations that have been entered into your projections.

You can set up the cash flow in Snap based on whether you prefer to enter:

- The amount of money the client saves to various investment accounts and assume they spend the rest. This is called manual cash flow management and it typically occurs before retirement.

- The amount of after-tax cash the client spends (i.e. their Base Expenses value). This is called automatic cash flow management and it typically occurs in retirement. Ensure the CFM Start Age is selected in the year you wish to begin entering a target value for Base Expenses.

- 2

-

Cash Flow before the CFM Start Age

The Base Expenses column displays the amount your client is assumed to be spending each year and it can't be edited directly, as indicated by the grey italic font. This value can only be updated by adjusting the other inputs such as contributions/withdrawals, debt payments, and insurance premiums prior to the CFM Start Age.

Using the first year of a projection for example, if an individual has $100k of Employment Income and they're paying $24,017 in Total Tax and Premiums, contributing $15,000 to their Financial Assets and paying $7,200 towards their Mortgage, the leftover cash is $53,783. The Base Expenses (Nominal column) displays this value.

- 3

-

Cash Flow after the CFM Start Age

Let's begin with the CFM Start Age selected as the first year of the projections. If we leave the Base Expenses annual amount set to $0, then the surplus cash will be deposited into the available Financial Assets according to the default logic starting in year one.

As indicated in the prior example, the surplus cash for the first year was $53,783. If we enter $0 for the first year's Base Expenses target value, then Snap will contribute that $53,783 to the available Financial Assets. If they are spending nothing on their lifestyle, they can save everything. Since there are already contribution overrides on the RRSP and TFSA accounts, these accounts are unavailable for automatic contributions and Snap contributes the entire surplus to the non-registered account.

If we wish to use the default logic, we can clear the manual contributions to the RRSP and TFSA and let Snap make those contributions automatically. To distinguish between contributions you have entered and those that Snap automatically populated, manual contribution/withdrawal overrides are highlighted with a yellow background.

The maximum RRSP and TFSA contributions are made, then the rest goes to the non-registered account.

Note that if you have no Financial Assets entered for this client, or if you have contribution overrides on all assets, Snap will contribute the surplus to the Cash Balance as shown here. Typically, you will want to ensure the Cash Balance is zero in your projections.

After clearing the manually entered contributions to allow automatic savings instead and ensuring a zero Cash Balance, the next step is to enter the client's target after-tax lifestyle requirements under Base Expenses (Real dollars). In this example, we have entered $54k for Base Expenses and run the scenario. The Financial Asset contributions now show an automatic contribution of $16,005 to the RRSP calculated as $100k Employment Income - $54k Base Expenses (Nominal) - $22,795 Total Tax - $7.2K Mortgage = $16,005.

- 4

-

A more formal definition of Cash Flow

Calculation without using the Taxable Income column:

AFTER-TAX CASH (ATC) = all Income from the Income page marked as taxable + Gov't Benefits - total tax - debt payments - additional expenses - contributions to non-registered assets - contributions to TFSA - contributions to registered assets (RRSP, LIRA, DCPP) - insurance premiums + other cash (non-taxable positive income columns, inflow of cash created by future debt or sale of a real asset) + withdrawals from non-registered assets + withdrawals from TFSA + withdrawals from registered assets (RRSP, LIRA, DCPP)

Note: OAS Clawback has not been included in this definition as it already lowers the OAS amount received.

Alternatively, if you want to factor in the Taxable Income column (already calculated for you), you can use the following definition:

AFTER-TAX CASH (ATC) = Taxable Income - total tax - debt payments - additional expenses - contributions to non-registered assets - contributions to TFSA - insurance premiums - interest on non-registered assets - dividend on non-registered assets - capital gains on non-registered assets - non-eligible and eligible dividend gross up + other cash (non-taxable positive income columns, inflow of cash created by future debt or sale of a real asset) + withdrawals from non-registered assets + withdrawals from TFSA

Note: In this 2nd definition, we need to separately account for interest, dividends, and the taxable portion of capital gains that are included in the Taxable Income column.

- 5

-

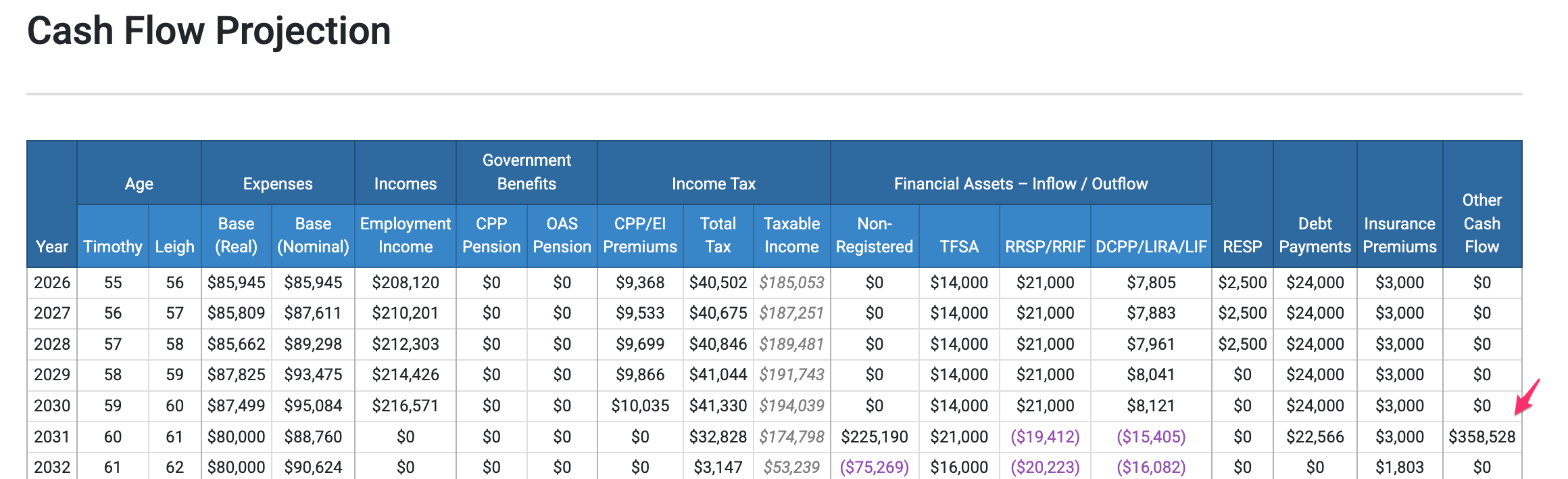

Cash Flow Projection Report page

This page is one of the most detailed report pages and our users have let us know it is one of the most impactful pages for their clients.

For a couple's projections you have the option to include a Cash Flow Projection for each spouse individually, and also for the couple.

Here is an example of the Combined Cash Flow Projection.

Here are a few notes about using the figures in this table to reconcile inflows and outflows.

- The Taxable Income column is provided for information purposes only and is therefore displayed in italic font. This figure is not used in the cash flow calculation.

- The Base Expenses Nominal dollar amount is the one calculations are based on in any given year.

- The Financial Assets inflow only includes the personal contributions to these accounts. (i.e. Group Account Employer contributions and RESP Grants are not included in this table since they don't affect the individual's cash flow).

In this example we can review the first year's cash flow to see reconciliation of inflows and outflows.

- Inflow in year 1 = $208,120 = Employment Income

- Outflow in year 1 = $208,120 = Nominal Base Expenses ($85,945) + CPP/EI Premiums ($9,368) + Total Tax ($40,502) + Personal Savings to TFSA, RRSP, DCPP, RESP ($45,305)+ Debt payments ($24,000) + Insurance Premiums ($3,000)

The Other Cash Flow column captures cash inflows and outflows that do not fit into other specific categories. It represents the net impact of these transactions on the plan and is used to simplify the table by bundling various transaction types together.

Here are some examples of what the Other Cash Flow value may represent in your projections (and this list is not exhaustive):

- Debt with a future start date (influx of cash)

- Sale of a real asset (positive amount)

- Purchase of a real asset (negative amount)

- Spousal RRSP contributions

- Transfers to a spouse for automatic TFSA top-ups

- Insurance proceeds

- Charitable donations

- Transfer of a positive Cash Balance or negative Cash Balance (debt) to the surviving spouse

In the projection displayed above, the Other Cash Flow in 2031 of $358,528 represents the proceeds of a real asset sale in that year.